Barron's highlights that 'stocks for the long-run' sometimes means a VERY long time (i.e. 30 years is not enough).

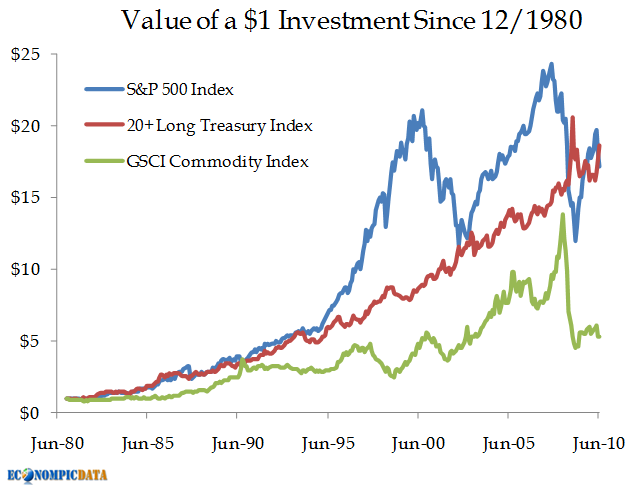

This hasn't been a short-term phenomenon. As Robert Kessler, head of the eponymously named Kessler Investment Advisors of Denver, points out, "perpetually maligned" 10-year Treasury zero-coupon STRIPS have outperformed both stocks (using the Standard & Poor's 500) and commodities (as measured by the GSCI total return index) over the past three, five, 10, 15 and 20 years.Chart of performance (these are total returns for each index) below:

This 30 year window has included a remarkable bond bull market and the most recent 10 year zero return stock market. But Barron's points out that while things are likely to revert back to stocks outperforming over the next 5, 10, and 20 years, there are plenty of drivers (outside of a global economic slowdown) that may cause Treasury bonds to outperform.

Bull markets in bonds, Kessler continues, last as long as 37 years. Yields peaked some 28 years ago in 1982, so they can continue to decline. Even at this relatively advanced stage of the Treasury bull market, he also points out that U.S. households' allocations to Treasuries is just 1.7%, compared to 4.6% in 1994 and 8.1% in 1952. That doesn't take into account proxies such as ETFs such as TLT, but the underweighting of Treasuries makes suggestion of a bubble less than credible.Source: Barclays Capital, GS, S&P

Speaking about equities for the LOOOOONNNNNGGGG Run...

ReplyDeleteMehra had a statistic about 10 years ago, in an update to the equity premium puzzle, that $1 invested in the US Stock Exchange in 1820 would be worth something like $0.5m, while $1 invested in Treasury bills at the same time would be worth about $220. (I hope I'm remembering the scale correct. The numbers were ridiculous anyway, so it was definitely a totally disproportionate return to risk.)

I have no idea how he corrected for survivor bias there, but I presume he was aware of it.

Just for fun, what are those annualized returns? I'm not good with backwards math.

ReplyDeleteStocks were still the better deal.

ReplyDeleteMost of the stock return would be capital gain, which is both deferrable and taxed at a lighter rate.

Much of the bond return would have been taxable income, with taxes based on your marginal income tax rate due every April 15.

depends if you're investing in a taxable account or not...

ReplyDelete10.1% vs 10.4% vs. 5.8%

ReplyDeleteIn fact, I think you will find that most of the return is re-invested dividends.

ReplyDelete