“Time solves most things. And what time can't solve, you have to solve yourself.” - Haruki Murakami

Recent research by GMO outlined that wide profit margins, low levels of inflation, subdued economic volatility, and low 10 year treasury rates have led to high valuations for both U.S. stocks and bonds. Yet irrespective of why valuations are high relative to history, what an investor pays for a dollar of earnings or a dollar of bond coupons directly impacts the forward return they receive. This is generally understood by investors who have accepted the likelihood that returns will be low over the next five or even ten years. What has been discussed less, or often dismissed outright by buy-and-hold long-term investors, is the similar challenge investors may face over much longer periods of time given high starting valuations.

- an investment that is down -50% in year 1, which then returns 10% each year for the next 29 years

- an investment that returns 10% each year for the full 30 years

For an investor looking to improve their outcome, there are a variety of options available, including:

- Search for Value: reallocate capital to segments of the US equity market (or outside the US equity market) that may be more attractive

- Identify Alpha Opportunities: rethink the value proposition of active management, especially within less efficient areas of the market

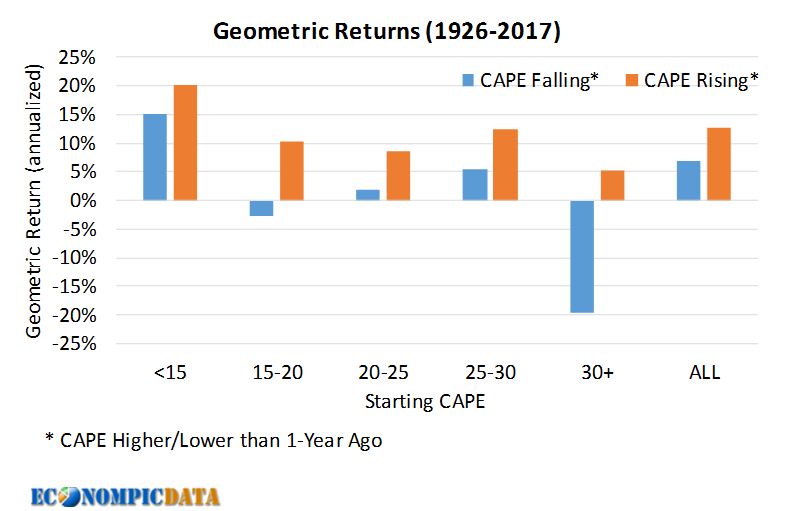

- Follow the Trend: utilize trend following to manage equity exposure

The first two options are familiar to most investors, but trend following may be less so. In a nutshell, trend following is simply a means of determining if you will own an asset based on its recent price history. One simple set of trend following rules are:

- If the S&P 500 Total Return Index > 12-Month Moving Average, Own Stocks

- Otherwise Own Bonds

Given this simple trend following model can never result in monthly outperformance vs the S&P 500 when the market is up, as the most it can own is 100% stocks, it will underperform during most bull markets relative to the S&P 500. However, it may still outperform a 60/40 portfolio in these environments as it is not weighed down by an allocation to bonds. Conversely, the strategy will outperform the S&P 500 in down markets over time and, importantly, it has the potential to side step a major market correction that impairs the compounding effect that has historically impacted long-term returns when valuations have been elevated (more on why trend / momentum works here).

The below chart updates the 30 year real growth of $1 with returns for this basic trend following strategy, comparing the returns generated to the original 60/40 buy-and-hold portfolio over similar periods.

While there are still material differences in the historical growth of $1 depending on the starting valuation, the trend following strategy generated dollar growth that was consistently higher than that of a 60/40 strategy and produced returns that were higher even at low starting yields than that of a 60/40 portfolio at much higher starting yield levels.

Buy and hold strategies work best when stocks and/or bonds are cheap. When valuations are extended and starting yields are low, an investor should look to allocate to cheaper areas of the global market, rethink the value proposition of active management, and/or be prepared to reduce stock market exposure if profit margins, inflation, volatility of GDP, or 10 year treasury rates (that pushed valuations higher) reverse course.