Source: BEA

Let's pretend for the time being that Forbes doesn't just stick their finger in the air and make up these valuations (an M&A professor of mine in business school shared that teams have a lot of influence in the Forbes' valuations, hence it shouldn't be a surprise that the Dodgers valuation is a whopping 75% higher than last year when the owner would have preferred a lower valuation while going through a divorce and higher valuation this year when selling the team).

The average Major League Baseball team rose 16% in value during the past year, to an all-time high of $605 million. In 2011, revenue (net of payments to cover stadium debt) for the league’s 30 teams climbed to an average of $212 million, a 3.4% gain over the previous season. But operating income (in the sense of earnings before non-cash charges and interest expenses) fell 13%, to an average of $14 million in part due to a 5.1% increase in player costs (including benefits and signing bonuses for amateurs), to $3.5 billion in 2011.

The Rolls-Royce of the RSN model is the New York Yankees, who own 34% of the YES Network. The Bronx Bombers are the most valuable team in baseball, worth $1.85 billion, tying them with the National Football League’s Dallas Cowboys for the top spot among American sports teams and placing them second in the world to Manchester United, the English soccer team worth $1.9 billion. YES generated a staggering $224 million in operating income and paid the Yankees a $90 million rights fee in 2011.

Ken Goldstein, economist at The Conference Board details:

“Recent data reflect an economy that improved this winter. To be sure, an unseasonably mild winter has contributed to many of the recent positive economic reports. But the consistent signal for the leading series suggests that progress on jobs, output, and incomes may continue through the summer months, if not beyond.”

The Rockefeller Institute details the continued, yet slower paced, growth in state tax collection in the fourth quarter:

Preliminary data for the October-December quarter of 2011 show further growth in state tax collections, with gains now coming for every quarter over two full years. However, such growth softened considerably in the second half of 2011. We will provide a full report on the October-December period after Census Bureau data for the quarter are available.

The Rockefeller Institute's compilation of preliminary data from all 50 states shows collections from major tax sources increased by 2.7 percent in nominal terms in the fourth quarter of 2011 compared to the same quarter of 2010. This is a noticeable slowdown from the 11.1 and 6.1 percent year-over-year growth reported in the second and third quarters of 2011 respectively.

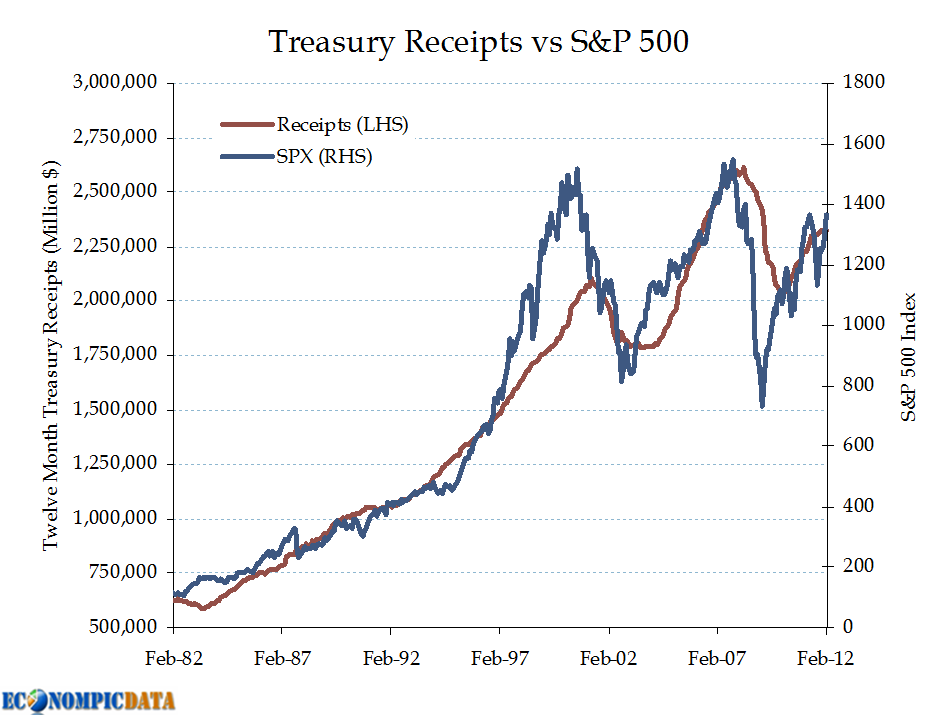

Pundits, bloggers, experts, etc... have been calling for a Treasury sell-off going on 3-4 years now (here is a post of mine from January 2009 on that exact subject.... and one from October 2010...and one from January 2012) so it is no surprise that the recent sell-off has brought the bears back out.

Statesman details:

The U.S. federal deficit was slightly smaller through the first five months of this fiscal year than the previous year. Still, the deficit is on pace to exceed $1 trillion for the fourth straight year, which could be an issue in this year's presidential election.

The Treasury Department said Monday that the deficit grew by $232 billion in February. That increased the imbalance through the first five months of the current budget year to $581 billion, or 9 percent less than the same period in fiscal 2011.

The Obama administration expects the deficit will reach $1.3 trillion when the fiscal year ends Sept. 30. The government ran a record deficit of $1.41 trillion in 2009 and a $1.29 trillion deficit in 2010.

BostonSportsHub provides a breakdown of how the NCAA bracket has performed by seed going back to 1997:

The first step in filling out your bracket is to understand the importance of seeding. Unless you are a complete novice to the religion that is March Madness, you know that in general the better the seed, the better the team. There are of course exceptions to this rule. At times the committee loses its mind, but in general the seeding is a fairly accurate representation of the quality of the teams. Here is how the seeds have performed on a round by round basis since 1997.

The Washington Post details:

U.S. employers added 227,000 jobs in February to complete three of the best months of hiring since the recession began. The unemployment rate was unchanged, largely because more people streamed into the work force. The Labor Department said Friday that the unemployment rate stayed at 8.3 percent last month, the lowest in three years.And hiring in January and December was better than first thought. The government revised those figures to show 61,000 an additional jobs.

The Federal Reserve released their quarterly Flow of Funds report today, which for a data nerd like me is just about as good as it gets. Unfortunately, not too much to report in terms of change, but I will highlight a few things that I've touched on in the past.

Marketwatch details:

Credit has risen for 5 straight months and fifteen out of the last sixteen months.

But analysts noted that all of the gain in January came from non-revolving debt, such as auto loans, personal loans and student loans.

These three categories combined for a $20.7 billion jump in January, the biggest gain since November 2001.

Once researchers exclude those loans to more accurately reflect the pool of borrowers who can actually be late, the delinquency rate more than doubled. In the end, 27 percent of the remaining borrowers were late on their payments, totaling about 21 percent of the aggregate loan balance.

Eddy Elfenbein tweeted this fun fact:

Take whatever today's $VIX is. Divide it by 3.46. That's the market's view of the 1 stand dev range +/- for the next 30 days. $$

Bloomberg details:

European retail sales unexpectedly rebounded from four months of declines in January, as growth in France helped to offset a drop in Germany.

Sales rose 0.3 percent from December, when they fell a revised 0.5 percent, the European Union’s statistics office in Luxembourg said today.

In Germany, Europe’s largest economy, retail sales fell 1.6 percent from December, when they advanced 0.1 percent, today’s report showed.

Marketwatch provides detail on a trend that will be important to keep an eye on:

Consumer spending is rising at tortoise’s pace for a very good reason: Incomes aren’t rising very much, especially after you adjust for higher prices.

Despite the good news on the jobs front over the past few months, personal incomes are barely keeping pace with inflation. Over the past six months, real disposable incomes are up just 0.6%, according to data released Thursday by the Commerce Department.

That’s slower than the population’s growth. On a per capita basis, inflation-adjusted, after-tax incomes are down 0.1% in the past year to $32,675 (measured in constant 2005 dollars).

Back on March 4th, 2008 EconomPic came to be with this sorry looking chart of CPI (seriously look at it... it's a joke). The point of the blog was simply to store charts that I regularly created to get a better sense of what was going on in this crazy world (timing couldn't have been better for material as the global economy was just about to blow up).

The blog has since evolved from a source for almost all relevant economic data (not sure how I found the time to post so often) to one that attempts to help digest the major economic data points and to share my 10,000 foot view on asset class valuation. So while my 15-20 post weeks will never return, the blog still hopefully provides readers with a better sense of what is going on in the world, while I more regularly post links and random thoughts over at Twitter.

I am incredibly thankful for the "in" that this blog has provided me to such a remarkable community of other bloggers and an audience of wonderful, thoughtful readers that make traditional media seem flat and out of touch. The fact that EconomPic just passed 2600 RSS subscribers is mind boggling. Giving back to this community is what provides me with the motivation to keep the blog going, despite the limited time a 3 month old son provides (for those that don't recall, I unsuccessfully "retired" last year... I simply couldn't stay away).

So thank you to everyone who has read or contributed, enabling EconomPic to be something more than a storage space for tacky charts.