The WSJ blog had a recent article The VIX Market Suggests It’s Not Yet Time to Buy the Dips outlining:

Typically, longer-dated VIX futures are more expensive than VIX futures expiring in the current month, as there’s a greater chance of stock swings over a longer time period. That makes for an upward sloping futures curve.

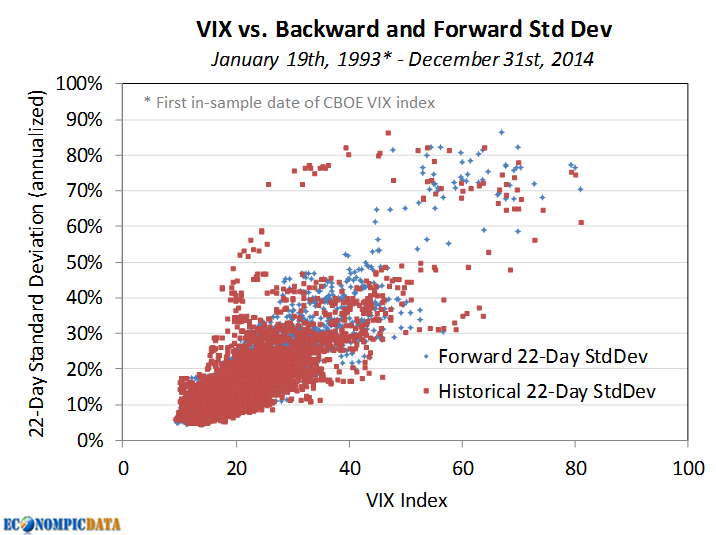

In times of stress, when investors are very fearful about the stock market over the next few weeks, they bid up the prices of short-dated futures more than the prices of the longer-dated futures. That phenomenon is known as “backwardation,” meaning a downward sloping futures curve.The article itself pointed to the relatively flat term structure (as of Friday), stating that an elevated VIX for the foreseeable future is a potential outcome. I've written in multiple iterations (here and here are two examples), that the VIX does a great job of predicting future levels of volatility AND risk-adjusted returns. What I'll take a look at now is whether the term structure adds additional insight (sneak peak... it just might).

The VIX Term Structure

I went into greater detail in a recent post about the VIX term structure (that was specific to trading VIX futures), where I introduced the VIX/VXV ratio (i.e. the Implied Volatility Term Structure or "IVTS"):

One way to make an allocation is to simply allocate to a long VIX futures position only when they have a tailwind vs. headwind. Simply calculate the term premium (a simple way is to use the VIX/VXV ratio - details of what that is by the great Bill Luby here) to determine contango or backwardation (in this case when the VIX/VXV is less than or greater than 100) and only allocate to UVXY when it's above 100. To put some numbers behind that statement, the average modeled daily performance of UVXY is -1.1% when the ratio is < 100 (2500 trading days) and 5.0% when the ratio > 100 (378 trading days) since 2004.So... in addition to simply looking at the level of the VIX (in this case whether the VIX is greater than 20), we also look at the levels of the IVTS (in this case if it's greater than 100).

The table below outlines the results of next day S&P 500 returns given the level and term structure of the VIX.

Some highlights... the geometric returns are broadly the same whether the VIX is above or below 20, but the volatility is MUCH lower at low levels of VIX (resulting in higher levels of risk-adjusted returns at low levels of the VIX). However, the addition of the IVTS signal shows a lot of interesting promise.

When both signs are in disagreement, returns are by far the best, with returns of 11.9% when the VIX > 20, but the IVTS < 100 and a whopping 105% when the VIX < 20 and the IVTS > 100. When both signals are telling investors to tread carefully (i.e. VIX > 20 and IVTS > 100), returns have been abysmal, with returns of -8.6% and volatility north of 40%.

Data Mined Model

Using the above insight to create a model that is absolutely data mined (yet may be interesting to look at going forward), we use the following rules:

- If VIX > 20 and IVTS > 100, go to aggregate bonds

- Otherwise, S&P 500

Something to keep an eye on as the warning signs are both currently flashing red.