Well, its been a full year since EconomPic Turned Two, which means EconomPic turned 3 today (unreal). As many a reader may remember, I begged and pleaded (or at least asked) a year back for help finding a job in San Francisco. After a lot of reader insight, help, and connections... nothing. Apparently there are easier things in life than finding a job 3000 miles away, during a jobless recovery, following a severe recession, when you don't know anyone in that city.

So, finally determined to move I had "the talk" with my "real job" (i.e. I gave my intention to move even if it meant walking away) and guess what? They are open to me (with some interesting arrangements) living in San Francisco after all. Who knew! So after 11 long, great, amazing years in New York City, I am headed west.

Which brings me to EconomPic. From this blogs March 4th, 2008 inception, through one of the more interesting / scary recessions of the past 70-80 years and subsequent rebound, blogging has been a pure joy. It provided me with an outlet to hone my "craft" (what I do here is very applicable to my "real" job) and it's taught me a TON about the world (it provided a huge incentive to "dig" into the data and my readers taught me more over the years than I imagined possible).

BUT, all good things must come to an end.

As long time readers are already well aware, my postings have been WAY down (i.e. lower quantity) and the posts I have done are much less commentary and much more day to day data in chart form (i.e. lower quality from templates I've created over years) the past 3-4 months. This is simply a result of what has been a lack of desire / lack of time to post (the "real" job has been taking up a lot more of my "free" time, the new arrangement will make that much worse). As a result, my three year anniversary seems like an ideal time to bow out. At least for now.

So, while I will not count out coming "out of retirement" if the desire returns or if the economy starts to go a new and interesting direction (or the new working arrangements don't work out), should that not happen I want to take this time to let all my royal readers over the past three years (2300+ RSS subscriber is still shocking) that I will miss you all.

-Jake

P.S. In the coming weeks, I plan to post a "Table of Contents" that will help direct readers through the 2224 posts (by topic) and data sources

Friday, March 4, 2011

EconomPics Turns Three... EconomRIP Edition

Employment Picture Improved

The economy added 250k jobs per the household survey and 192k per the establishment survey (222k private jobs) on a seasonally adjusted basis. Non-seasonally adjusted, the economy added almost 500k jobs per the household survey and 810k per the establishment survey. Not a blow out, but a definitive improvement.

Source: BLS

Thursday, March 3, 2011

Getting There

I'm expecting an above consensus employment number tomorrow (i.e. 250+), as I think January's employment figure was artificially low due to weather and past data missing the (albeit small) turn.

We shall see...

Source: DOL

Tuesday, March 1, 2011

Autos Over the Long Term

4 years later we're making some real progress in the economy across the board, but showing how deep the dive was... auto sales are still ~20% below the level seen four years ago.

More telling. Lots of US autos near the bottom and only one (Cadillac) with more sales than pre-crisis.

Source: Autoblog

Manufacturing Expands at Fastest Pace Since 1983

- "A continued weak dollar is increasing the cost of components purchased overseas. It is going to force us to increase our selling prices to our customers." (Transportation Equipment)

- "We continue to see significant inflation across nearly every type of chemical raw material we purchase." (Chemical Products)

- "Our plants are working 24/7 to meet production demands." (Fabricated Metal Products)

"Prices continue to rise, while business limps along at last year's pace." (Nonmetallic Mineral Products) - "Overall demand is off 10 percent." (Plastics & Rubber Products)

Monday, February 28, 2011

More on Personal Consumption

In response to my post Something Sustainable reader Tom Lindmark commented:

As I understand the numbers, real PCE declined 0.1% and disposable income was up only 0.1% if you net out the effects of the reduction in withholding taxes and the expiration of Making Work Pay.From a quick look it appears taxes actually rose $55 billion in the period in nominal terms (not sure real terms), but Tom is correct that real PCE declined in January, but predominantly due to a decline in real energy consumption (though nominal consumption remains high). This can be seen in the below chart that compares components of real PCE over 3 and 12-months. Notice that real consumption has declined in all areas, with the exception of services and energy.

Source: BEA

Something Sustainable

Source: BEA

Friday, February 25, 2011

Thursday, February 24, 2011

Durable Goods Orders Up... Not Exactly What it Seems

Marketwatch with the details:

Orders for U.S.-made durable goods rose 2.7% in January on stronger demand for civilian aircraft, the Commerce Department reported Thursday. The increase in total orders was very close to the 2.5% gain that was the consensus forecast of economists polled by MarketWatch. This is the first increase in durables in four months. Orders for December were revised up sharply to a decline of only 0.4% from the prior estimate of a 2.3% decline.Nondefense aircraft orders were up a whopping 4900% (after a crash in December). Without nondefense aircraft, orders were actually down a bit (though smoothing December, durable goods orders were actually up 2% ex nondefense aircraft).

Source: Census

Tuesday, February 22, 2011

Growing Secular Volatility?

The Big Picture notes that today's S&P 500 performance (-2.05%) was the worst in 6 months.

More interesting is the frequency of -2% days over the past 60 years. The chart below shows the number -2% days over 100 trading day periods over that time. As can be seen, while we had a "great moderation" from October 2003 through February 2007 (a whopping 850 trading days without a 2% down day), the frequency seems to be growing steadily since the early 1970's when there are periods of market duress.

Source: Yahoo Finance

Thursday, February 17, 2011

Case Shiller Price Index

Haven't posted this in a while...

As I've previously detailed, CPI may not reflect actual price levels for an individual who:

- does not own a home

- would like to own a home

- will likely soon buy a home

Why? Full details here, but in a nutshell the CPI measure includes a 'home owners equivalent rent', which has not fluctuated nearly as much as the actual home price level in recent years (both on the way up and on the way down).

The below shows headline CPI vs. a "Case Shiller Price Index" that swaps in the actual home price levels (per the Case Shiller) for the equivalent rent figure (assuming a constant ~25% weighting of owners equivalent rent within the broader index and flat price levels in December and January).

By this measure we see much higher inflation pre-crisis than reported, much greater deflation post-crisis, and the potential beginning stage of another divergence.

Source: BLS / S&P

Leading Indicators Up Slightly in January

Marketwatch details:

The economy's expansion is expected to continue in coming months, though current conditions, which are slowly improving, remain weak, the Conference Board said Thursday as it reported that its leading economic index rose 0.1% in January.

Six of the 10 indicators included in the LEI made positive contributions in January, led by the interest rate spread. The largest negative contribution came from building permits. Economists polled by MarketWatch had expected the overall index to rise 0.2% in January.

Source: Conference Board

Wednesday, February 16, 2011

Producer Prices Continue to Rise... Feeding into Core

Bloomberg details:

Wholesale costs in the U.S. increased for a seventh consecutive month in January, led by higher prices for fuel.

The producer price index rose 0.8 percent, Labor Department figures showed today in Washington. The figure matched the median forecast in a Bloomberg News survey. The so-called core measure, which excludes volatile food and energy costs, rose 0.5 percent, the biggest rise since October 2008.

Source: BLS

Tuesday, February 15, 2011

Deficit Financing

The AP details:

Not since World War II has the federal budget deficit made up such a big chunk of the U.S. economy. And within two or three years, economists fear the result could be sharply higher interest rates that would slow economic growth.

The budget plan President Barack Obama sent Congress on Monday foresees a record deficit of $1.65 trillion this year. That would be just under 11 percent of the $14 trillion economy — the largest proportion since 1945, when wartime spending swelled the deficit to 21.5 percent of U.S. gross domestic product.

The concern is what happens when rates begin to rise, if there is not offsetting growth and/or inflation to keep costs low on a relative basis. Back to the AP:

"The moment when markets react negatively to our budget deficit cannot be known in advance, but we are absolutely in the danger zone," says Marvin Goodfriend, an economics professor at Carnegie Mellon University's Tepper School of Business.

Higher interest rates would also raise interest payments on the federal debt. It would be costlier for the government to finance its operations. The interest payments themselves could then make the deficit increase, creating a vicious cycle.

Retail Sales Up... Inflation Edition

Marketwatch details:

The biggest increase in sales took place at gas stations, grocery and liquor stores, auto retailers and online and catalog merchants. Sales fell at clothing and building-supply stores.It's not a surprise that this was the result in a period when commodity prices (in the form of food and energy) spiked. Removing these volatile sectors of the retail market and we get a much more mundane 0.04% increase in the month.

Monday, February 14, 2011

Natural Rate of Unemployment

Bloomberg details:

The new “normal” unemployment rate may now be 6.7 percent, rising as much as 1.7 percentage points from 5 percent before the recession began, according to researchers at the Federal Reserve Bank of San Francisco.That's one explanation (and I can't disagree with the above facts), but perhaps the "natural" rate of unemployment was never as low as it appeared from the late 80's through late 00's either.

High rates of long-term joblessness, extended unemployment benefits and a mismatch of skills between workers and available jobs may be impeding a return to the previous level, said John Williams, the bank’s research director, and research associate Justin Weidner in a paper released today.

Source: BLS

Budget Still Out of Control

You can argue that the dialogue around cutting the budget going forward is a good start, but increasing the deficit to $1.6 billion from an initial $1.4 billion is the wrong direction. Bloomberg details:

President Barack Obama will send Congress a $3.7 trillion budget that would reduce deficits by $1.1 trillion over a decade, setting up a battle with Republicans who have already deemed the plan insufficient to reduce federal debt.

The deficit for the current fiscal year is forecast to hit a record $1.6 trillion -- 10.9 percent of gross domestic product -- up from $1.4 trillion the administration estimated previously, according to documents released this morning by the administration.

Source: GPO Access

Sunday, February 13, 2011

Japan's Lost Decade(s)

BusinessWeek details the latest:

Japan’s gross domestic product fell less than estimated in the fourth quarter in a pullback that may prove temporary as overseas demand revives production after the nation fell behind China as the world’s second-largest economy.

The annualized 1.1 percent drop in GDP in the three months through December was driven by a slowing in exports and fading of government stimulus programs, Cabinet Office figures showed today in Tokyo. The median forecast of 26 economists surveyed by Bloomberg News was for a 2 percent drop.

Source: ESRI

Tuesday, February 8, 2011

Monday, February 7, 2011

Has Re-Leveraging Begun?

Non-revolving credit is now at new all-time highs and the revolving cliff dive has hit a bottom (i.e. it is turning up... for now).

Source: Federal Reserve

On the Prospects of G

The chart below shows the annual change in government spending and investment since 1960 (left hand side) and contribution to overall GDP growth (right hand side).

The takeaway? The government sector has been a consistent source of growth (positive in 36 out of 37 years), but with states acting like Europe (i.e. austerity) and the need to cut back, expect this to reverse course in the years to come.

Source: BEA

Friday, February 4, 2011

EconomPics of the (Since my Last EconomPics of the) Week

Economic Data

On the Job Non-Recovery

ISM Services Growth at Fastest Pace in 5 1/2 Years...

ISM Manufacturing Up for 20th Straight Month

The Importance of Small Business

Productivity Continues Hot Streak

European Retail Sales Decline

Auto's Continue Rebound

Chicago PMI Points to Heating Economy / Input Pric...

GDP Growth at 3.2% in Q4

Consumer Confidence Improves in January

Europe's Industrial Rebound: The Power of Mean Reversion

Housing Starts Quite Low

Empire Manufacturing Outlook at Seven Year High

Still Too Much Capacity

Asset Classes

Odd Month

The Bulldog Bubble

Taking a Look at the Cash Hoarders

Dividend vs. Buyback Yield... The Importance of Timing

Case Shiller Index Points to Housing Double Dip

China Hearts Silver... Market Top?

Housing Market Drives Leading Economic Indicators?...

The Equity Market is in Trouble... J-E-T-S Edition...

China Still NOT Selling Treasuries

And your video of the week... Passion Pit with Little Secrets

On the Job Non-Recovery

The disappointing jobs data this morning, perhaps due to weather, detailed by Bloomberg:

The U.S. jobless rate unexpectedly fell in January to the lowest level in 21 months, while payroll growth was depressed by winter storms.As we've detailed for some time the improvement in the unemployment rate is due to the denominator (in the unemployed / labor force equation) dropping off a cliff. The chart below details this phenomenon over the past twelve months according to the household survey. As can be seen, jobs are finally being added (~900 thousand), but during a time when the population of working age individuals in the U.S. grew by ~1.9 million. Add in a drop in the labor force (~420k) and you get ~2.3 million MORE individuals than last year that could be working, not working.

Unemployment declined to 9 percent from December’s 9.4 percent, the Labor Department said today in Washington. Employers added 36,000 workers, short of the 146,000 median gain projected by economists in a Bloomberg News survey.

We need to do better than this.

Source: BLS

Thursday, February 3, 2011

ISM Services Growth at Fastest Pace in 5 1/2 Years

ecPulse details:

The Institute for Supply Management released today the ISM services index, where the ISM Services index rose in January to 59.4 from the prior reported estimate of 57.1 and well above the expected estimates of 57.2. The services sector expanded in January at the fastest pace since August 2005.

The business activity index rose to 64.6 from 62.9, while the prices paid index rose to 72.1 from 69.5, new orders increased to 64.9 from 61.4, while the employment index rose to 54.5 from 52.6, new export orders slightly eased to 53.5 from 56.0 and imports increased to 53.5 from 51.0.

Productivity Continues Hot Streak

Bloomberg details (bold mine):

The productivity of U.S. workers unexpectedly increased in the fourth quarter at a faster rate as companies sought to contain costs.

The measure of employee output per hour rose at a 2.6 percent annual rate, compared with a revised 2.4 percent gain in the previous three months, figures from the Labor Department showed today in Washington. Economists projected a 2 percent advance, according to the median forecast in a Bloomberg News survey. Labor expenses fell for fifth time in six quarters.

“There is a good chance that productivity will slow further this year, as firms are increasingly forced to hire more workers to expand output,” Paul shworth, chief U.S. economist at Capital Economics Ltd. in Toronto, said in a note to clients. “That is good news for the unemployed.”

Source: BLS

European Retail Sales Decline

Euro zone retail sales unexpectedly fell in December with equal declines in food

and non-food sectors, a sign that consumers in the single currency bloc were reluctant to splurge even in the key holiday period.

The European Union's statistics office Eurostat said on Thursday retail sales in the 16 countries using the euro fell by 0.6 percent month-on-month, for a 0.9 percent year-on-year decline.

Economists polled by Reuters had expected a 0.5 percent month-on-month rise and a 0.2 percent increase year-on-year.The new data came while European Central Bank policymakers met to decide on interest rates. Economists said they did not expect weak retail sales to prevent the ECB from issuing a warning on inflationary pressures.

Wednesday, February 2, 2011

Tuesday, February 1, 2011

ISM Manufacturing Up for 20th Straight Month

Marketwatch details:

Conditions for the nation's manufacturers improved for the 20th straight month, the Institute for Supply Management reported Tuesday. The ISM index rose to 60.8% in January from 58.5% in December. This is the highest level of the factory index since last May. The report was much stronger than expected. The consensus forecast of estimates collected by MarketWatch was for the index to remain steady at 58.5%.

Readings above 50 indicate expansion. Below the headline, the report was also strong. The key employment index improved to 61.7% in January from 58.9% in December. New orders jumped to 67.8% in January from 62% in the prior month. Input prices soared in January. The price index jumped to 81.5 from 72.5 in the prior month.

Source: ISM

Monday, January 31, 2011

Odd Month

Justification for the below?

- Risk on / reflation in the developed world (continued dollar sell-off)

- Brakes thrown on in emerging market world

- Sell-off in rates across the board

- Gold and oil off because... who knows

Source: Google Finance

Chicago PMI Points to Heating Economy / Input Prices

Bloomberg detailed:

Businesses in the U.S. expanded in January at the fastest pace since July 1988, indicating the world’s largest economy has momentum at the start of the year.

The Institute for Supply Management-Chicago Inc. said today its business barometer rose this month to 68.8 from 66.8 in December. Figures greater than 50 signal expansion, and economists projected the gauge would slip to 64.5, based on the median estimate in a Bloomberg survey.

Source: ISM

Friday, January 28, 2011

GDP Growth at 3.2% in Q4

Pretty wild release. HUGE positive impact (more than 3%) by improvement in net exports. HUGE positive impact (more than 3%) by consumption (strong demand in durable and non-durable goods). HUGE negative impact (almost 4%) by inventory liquidation to meet final demand vs. new production.

My initial thoughts? I've been looking for a bump in aggregate global demand and the jump in consumption and net exports is a good sign. In addition, the fact that we have met final demand by depleting inventories, once again feeds the cycle that businesses have to ramp up production to meet final demand going forward (which will positively impact future economic growth).

Source: BEA

Wednesday, January 26, 2011

The Bulldog Bubble

Random? Yes, but I like dogs...

The American Kennel Club (hat tip Skip) details:

This year’s list included some shakeups in the top 10 – the Beagle overtook the Golden Retriever for the 4th spot and the Bulldog, who has been steadily rising up in rank, took 6th place away from the Boxer, who dropped to 7th in 2010.

"Not since the early 20th Century has the Bulldog enjoyed such sustained popularity," said AKC Spokesperson Lisa Peterson. "‘Bob’ was the first AKC registered Bulldog in 1886, and today the breed enjoys its highest ranking in 100 years at number 6."

Source: American Kennel Club

Taking a Look at the Cash Hoarders

The Huffington Post details the top 11 cash hoarders.

Below is a chart of the cash levels for 10 of the 11 (I excluded GM as they don't have 12 month's of positive earnings), the earnings yield of each company (defined as the inverse of the P/E ratio), and the adjusted earnings yield that backs out the cash from the corporation's market value to determine the earnings power of the company less cash (normally you would have to account some earnings to the cash, but in the current environment, that is minimal).Instead of building plants or hiring workers, corporate America is clinging to its cash.Companies are sitting on $1.93 trillion in cash and liquid assets, the highest level since 1959, the Wall Street Journal reports.

With high unemployment and families still limiting their spending, corporate America is backing away from expansion. But with interest rates on the heaps of cash so low, that $1.3 trillion might as well be stuffed in a mattress.

Note that all cash data is directly from Huffington Post and Google Finance (I did not go through financials) and is presented without analysis or determination as to whether any of the figures should be adjusted for any reason. That said, if the cash is returned to investors via dividend or buyback OR the cash is put to good use, corporations appear cheaper than they might first appear.

Tuesday, January 25, 2011

Dividend vs. Buyback Yield... The Importance of Timing

Professor Damodaran (via World Beta and Abnormal Returns):

S&P's most recent update indicates that US companies, after a pause for about a year after the banking crisis, are back in the buyback game. In the third quarter of 2010, the S&P 500 companies bought back almost $ 80 billion of stock, up 128% from the third quarter of 2009.The below chart shows the dividend yield (dividends divided by the S&P 500's market cap) and buyback yield (buybacks divided by the S&P 500's market cap) on a quarterly basis (annualized) going back to 2004.

Professor Damodaran does provide some rationale / discussion into why the trend has moved to buyback vs. dividend:

- Manager compensation: buybacks increase the price of stock for manager option grants

- Uncertainty about earnings: buybacks are a lot more flexible than a steady dividend

- Changing investor profiles: investors that are more focused on stock price

- Higher earnings per share: less shares outstanding = more earnings per share (tested here)

Consumer Confidence Improves in January

Marktetwatch details:

An index of U.S. consumer confidence jumped to 60.6 in January, reaching the highest level since May, with more consumers optimistic about income and jobs, as well as current business conditions, the Conference Board reported Tuesday.Note that this does not mean consumers are confident, just that their confidence has improved. Taking a look at the details behind the index we see an improvement across the board, but from very low levels.

Source: Conference Board

Monday, January 24, 2011

Europe's Industrial Rebound: The Power of Mean Revision

RTT News details:

Eurozone industrial new order growth quickened in November, led by Portugal, Finland and Germany, official figures showed Monday. Industrial orders rose 2.1% month-on-month in November, after rising 1.4% in October, the European Union Statistical office Eurostat said. On an annual basis, industrial order growth accelerated to 19.9% from 14.8% recorded in the preceding month. The rise exceeded the 17.5% increase economists had forecast.The below charts show that much of this is purely a rebound off lows, with a relatively strong relationship between those reporting strong results in 2010 off of lower figures in 2009.

Source: Eurostat

Friday, January 21, 2011

China Hearts Silver... Market Top?

FT Alphaville reports (via Bullion Vault dealers):

Looking at China’s latest import data, 2010 saw silver imports (net of exports) rise four-fold from 2009 note analysts at Mitsui in London – a total of 3,500 tonnes.

A heavy seller of silver bullion after lifting the state’s 50-year monopoly in 2000, China was a net export of 3,000 tonnes as recently as 2005.

Is this support for the massive 80% year over year jump in the price of silver under the belief that China will continue to be a huge buyer of silver? Or is this a sign that the price is bubblicious and investors should be concerned that China's economy will be forced into slow down mode (thus less net purchases) following the recent strong print in both growth and inflation?

Source: Yahoo Finance

Thursday, January 20, 2011

Housing Market Drives Leading Economic Indicators?

Bloomberg details:

The index of U.S. leading economic indicators increased in December more than forecast, a sign the recovery will gather steam in the new year.And the biggest driver of that growth...

The Conference Board’s gauge of the outlook for the next three to six months rose 1.0 percent after a 1.1 percent gain in November, the New York-based group said today. The December reading, the sixth consecutive monthly increase, exceeded the 0.6 percent gain in the median forecast of economists surveyed.

- The improving job market? Nope.

- The rising equity market? Nope.

- The steep yield curve? Nope

The level of permits in December, excluding the recent downturn, was the lowest figure since records began in 1960 (when the U.S. population was about 40% smaller), yet this was the biggest driver of the leading indicators.

Why?

Addition by the elimination of subtraction.

In other words, it can't get any worse than this, thus it can only get better (much more detail on this over at Calculated Risk).

Source: Conference Board

The Equity Market is in Trouble... J-E-T-S Edition

Floyd Norris (via The Big Picture):

Consider the performance of the Standard & Poor’s 500 in 1969, the year the Jets won their only Super Bowl. It was down 11.4 percent.

Contrast that to the market’s performance after victories by any of the other teams still in contention. The market has never gone down after any of them won the Super Bowl.

Since:

A) The market has "always" gone down when the Jets win

B) The Jets will win (warning: the last time I was this confident they lost by more than 40)

C) The market will go down

Or something like that...

Wednesday, January 19, 2011

Housing Starts Quite Low

Housing market optimists will blame this partially on December weather. Broader optimists will point out that low levels of new construction will help clear the existing inventory. Those looking for the housing market to contribute towards the economic recovery (outside of addition by the elimination of subtraction) will be disappointed.

Tuesday, January 18, 2011

China Still NOT Selling Treasuries

Back in February of last year I detailed that China was NOT selling Treasuries when the "experts" in the media said they were. TIC December 2009 data initially stated Chinese holdings totalled a bit more than $700 billion, down from summer '09 levels. I made the case that these purchases were actually being made through the United Kingdom (more here). They were. The result is that China's December 2009 holdings were revised upward by $200 billion.

"Experts" in the media would have learned their lesson by now right?

To the Financial Times:

The FT was joined by the WSJ, CNN, and Marketwatch amongst others getting it wrong. Bloomberg got it right here, but wrong here.China and Russia were the major sellers of US Treasuries in November as bond yields surged sharply higher that month, according to the latest government data.

The US Treasury reported on Tuesday that private investors sought more dollar-denominated stocks and bonds in November than October, offsetting record sales by foreign governments.

Facts:

1) Journalist do not read EconomPic

2) China is NOT selling Treasuries

Source: Treasury

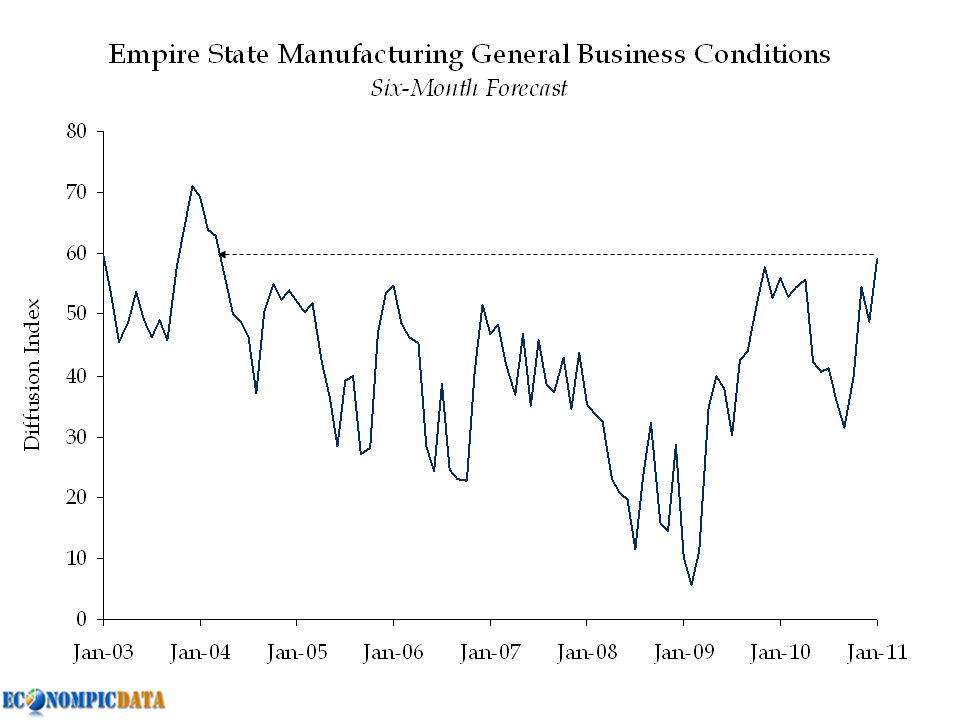

Empire Manufacturing Outlook at Seven Year High

Will this be enough for them to spend some of that cash hoard?

Source: NY Fed

Still Too Much Capacity

The below chart shows that capacity utilization in the system is slowly recovering, but remains remain very low.

This in part explains why core inflation remains muted, even with the recent commodity spike.

Source: Federal Reserve / BLS

Friday, January 14, 2011

EconomPics of the Week (1-14-11)

This be called EconomPics of the year to date, but doesn't sound as good.

Assets / Financial Markets

China Owns Lots of Paper

A Strong 2010 for Hedge Funds

The History of Corporate Bonds

Trading Day #1 of 2011 = Risk On

Realized 20-Day Vol at 39 Year Low

Debt

The Federal Debt Spike

More on the Federal Debt

An Even Uglier Federal Debt Chart

Economic Data

Mind the Gap

PPI Hits Four-Handle

Employment Picture: Getting There... VERY Slowly

Employment Higher, but Disappoints

An Employment Report We've Been Waiting For

ISM Services Strong in December

Other

The iPhone was a Huge Success...

Bernanke: 2010 Fund Manager of the Year

And your video of the week... Black Keys with Tighten Up. And you thought Ohio was worthless.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}