Lawrence Hamtil recently shared a Vanguard paper with me that was surprising given it indicated the trailing twelve month price-to-earnings ratio "TTM P/E" was nearly as strong a predictor of forward 10-year equity returns as the cyclically adjusted price-to-earnings "CAPE" ratio going back to 1926. My assumption had been that the CAPE ratio (which uses smoothed 10-year real earnings) would be the much better of the two ratios given it reflects the longer-term earnings power of companies within the index, rather than the (potentially at times) cyclical peak.

This post will dig into:

- the historical relationship between the TTM P/E and CAPE ratios and forward returns

- the historical relationship between the TTM P/E and CAPE ratios, and how that relationship has changed in recent years

- how these ratios may potentially be used together to help predict shorter term market performance

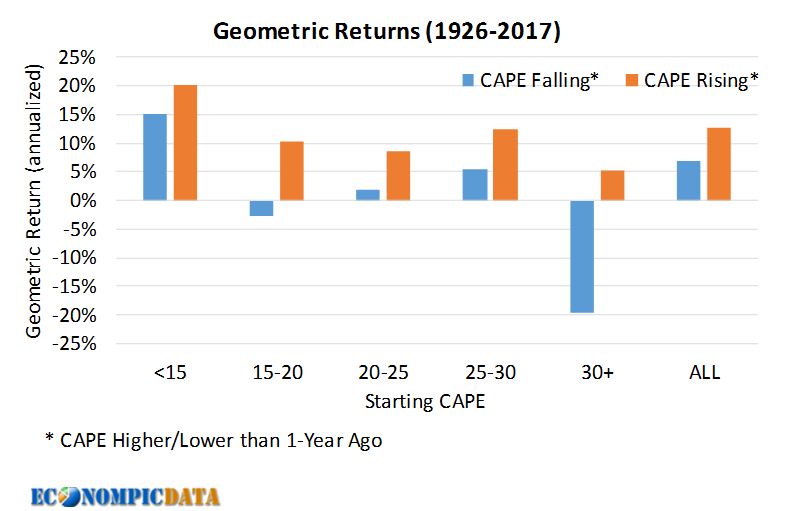

Backdrop: The Surprising Predictive Power of TTM P/E

While perma-bears seem to enjoy highlighting metrics (debt, rates, growth rates, etc...) that have no predictive power for either short or long-term forward equity returns, valuations themselves have mattered. As I’ve highlighted in previous posts, higher valuations (as defined by an elevated CAPE ratio) have historically resulted in lower long-term forward returns. Vanguard replicated this result for trailing P/E, which surprised me given the backward looking / shorter-term / cyclical nature of the TTM earnings component in the denominator of the P/E ratio.

Per Vanguard:

We confirm that valuation metrics such as price/earnings ratios, or P/Es, have had an inverse or mean-reverting relationship with future stock market returns, although it has only been meaningful at long horizons and, even then, P/E ratios have “explained” only about 40% of the time variation in net-of-inflation returns. Our results are similar whether or not trailing earnings are smoothed or cyclically adjusted (as is done in Robert Shiller’s popular P/E10 ratio).

Given my need to replicate anything I see to personally believe, the below charts replicate this analysis with a scatter plot for each updated through May 2018 (the Vanguard piece is through 2011) using data from Shiller (the dotted line shows the ratio as of May 2018). We see both relationships remain strong, though the CAPE’s predictive power has improved quite a bit (more on that below) since 2011.

The Changing Relationship Between the CAPE and TTM P/E

The reason the CAPE shows a higher predictive power in updated results is due to the divergence of the two ratios leading up to and through the global financial crisis “GFC” when earnings collapsed, causing the TTM P/E to spike, which in turn made the US equity market seemingly more expensive as it sold off.

Meanwhile the US equity market appeared quite cheap on a CAPE basis (it hit a ~30 year low), which turned out to be the correct signal. In the following chart we can see the close relationship between the two ratios following the Great Depression through late 1990’s, then the divergence seen first during and after the technology bubble (note the chart stops at 50 to show the data more clearly, but the TTM P/E spiked to 86 in October 2008).

As a result, in the more recent periods that capture the Internet Bubble and/or GFC at the back, middle, or the front of a 10 year rolling period, the CAPE has been extremely predictive (89%), while the TTM P/E has been less so

The Potential Use of the CAPE and TTM P/E to Make Allocation Decisions

The following chart shows the difference between the two ratios over time. We can see that for a ~60 year window following the Great Depression to the beginning stages of the Internet Bubble they moved together closely. We can also see the more recent divergence.

And this is where I think things get interesting and potentially less intuitive.

Historically, when the CAPE was elevated (meaning markets were potentially at risk from a valuation standpoint) and the CAPE > TTM P/E (meaning recent earnings in the TTM denominator are higher than the smoothed 10-year real earnings), forward short-term performance has been just fine. It's when the CAPE was elevated (again… meaning markets were potentially at risk from a valuation standpoint) and CAPE < TTM P/E (meaning recent earnings have lagged the smoothed 10-year real earnings) that short-term performance hasn't just been poor, but outright negative.

In fact, looking back at the chart above we can see the CAPE ratio exceeded the TTM P/E by a substantial margin before the major market corrections of the Great Depression, Internet Bubble, and GFC, but when the CAPE flipped below the TTM P/E is when each sell-off really took hold. Note that in the Great Depression the US equity market continued to sell-off even after the CAPE got to seemingly attractive levels.

My takeaway from all of this remains that forward long-term returns are likely to be low relative to history (both CAPE and TTM P/E point to that likelihood), while the shorter-term outlook looks better. Investors tactically holding US stocks may be well served by what has historically been strong equity performance in elevated valuation environments when current earnings remain strong and/or the upward trend of the market stays intact. But buyer beware... should either earnings or the positive trend of the market shift, current valuations increase the risk that this may end up viewed as a period of calm before the storm.