The bull's case has been that the emerging market growth will more than make up for stagnant growth in the developed world. Data coming out of China doesn't do anything to counter that argument. Reuters details:

Chinese exports in May grew about 50 percent from a year earlier, sources said on Wednesday, a figure that blew past expectations and fuelled a rise in stock markets globally.

The key Chinese stock index .SSEC, which had been in negative territory, jumped 2.8 percent as the strong export growth reassured investors who have been worried that the European debt crisis would weigh on the global economy.

Exports, which are scheduled to be reported as part of broader trade data on Thursday, had been expected to rise 32.0 percent year-on-year in May after recording a 30.5 percent pace in April.

And that is not where China's impact on a global recovery ends. The Washington Post reports:

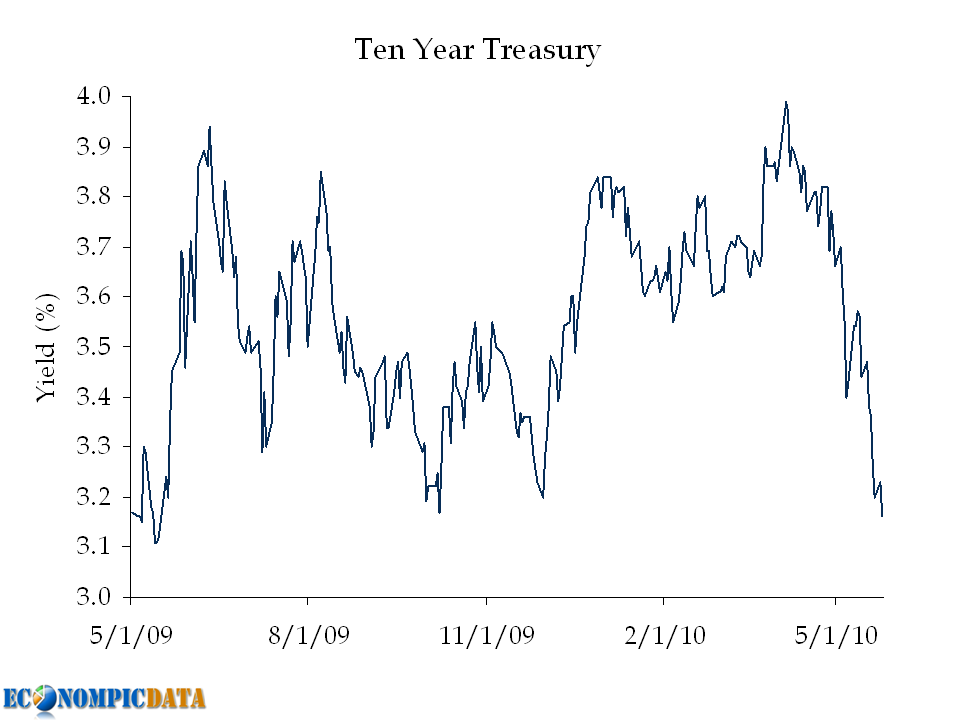

Source: HaverNearly bankrupt and sullied in the eyes of foreign investors, Greece is moving to rebuild its economy by tapping the deep pockets of another ancient civilization: China.

Spurred on by government incentives and bargain-basement prices, the Chinese are planning to pump hundreds of millions -- perhaps billions -- of euros into Greece even as other investors run the other way. The cornerstone of those plans is the transformation of the Mediterranean port of Piraeus into the Rotterdam of the south, creating a modern gateway linking Chinese factories with consumers across Europe and North Africa.

The port project is emerging as a bellwether for Greek plans to pay down debt and reinvent its broken economy by privatizing inefficient government-owned utilities, trains and even casinos. This week, the Chinese shipping giant Cosco assumed full control of the major container dock in Piraeus, just southwest of Athens. In return, the Chinese have pledged to spend $700 million to construct a new pier and upgrade existing docks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![18% [up from 8%]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEh4Jn7bZ6OClO-cKmEmwPGJwpUjy50MhsJknYMwCBAWdre-AizdHGmV-o0Ek9WmNDFxRd6cY2oEOpSbOSnWVUCaEKP2-h-CREMZ224y0KhlRNwgtaedSDEhShsUdZF1PwtQEcerbXUEWQ/s1600-h/OfficeVacancyQ3.jpg){kind=link}