Source: Yahoo Finance

Thursday, August 4, 2011

Here We Go Again

As I've detailed over the last month, market volatility appeared suppressed due to all the liquidity thrown at the problems:

Volatility is finally picking up and I want NO part of it. So today, I closed out most of my long volatility positions (with the exception of those tied to commodities and Treasuries... I think we're going one way or the other here) and happy to sit on cash until dislocations become wider or markets calm down a bit. We seem to be are treading in awfully familiar territory, which brings to mind a great Operation Ivy song.

Here We Go Again

Monday, August 1, 2011

Manufacturing Rebound Stalls in July

Peter Boockvar (via The Big Picture) details:

July ISM manufacturing index at 50.9 was well below expectations of 54.5, down from 55.3 in June and the weakest since July ’09. New Orders fell below 50 at 49.2 for the 1st time since June ’09. Backlogs fell 4 pts to 45 and importantly, employment fell 6.4 pts to 53.5, the lowest since Dec ’09. Export Orders did rise 0.5 points to 54, but off the slowest since July ’09.Inventories at both the manufacturers and customer levels fell. Prices Paid fell 9 pts to 57, the lowest since July ’10. Of the 18 industries surveyed, just 10 saw growth. ISM summed up July with this, “despite relief in pricing, however, several comments suggest a slowdown in domestic demand in the short term, while export orders continue to remain strong.”Bottom line, we saw softening in almost all of the regional manufacturing surveys over the past few weeks with today’s only question being to what degree. As I mentioned last week, what today and last week also proves, its the economy that is driving markets and the politics of debts and deficits are just awful noise in the background right now.

Friday, July 29, 2011

EconomPics of the... Since the Last Time

It's been a long while since an EconomPic recap, so here goes...

Asset Classes

Economic Data

Random

And the EconomPic video of the week... a sick rendition of a great song. ThePETEBOX with a cover of the Pixies Where is My Mind?

Turning Japanese

I've recommended Steve Keen's piece The Roving Cavaliers of Credit before, but I highly recommend it for those that think inflation remains a concern.

Source: BEA

Rewind: On the Value of Treasuries

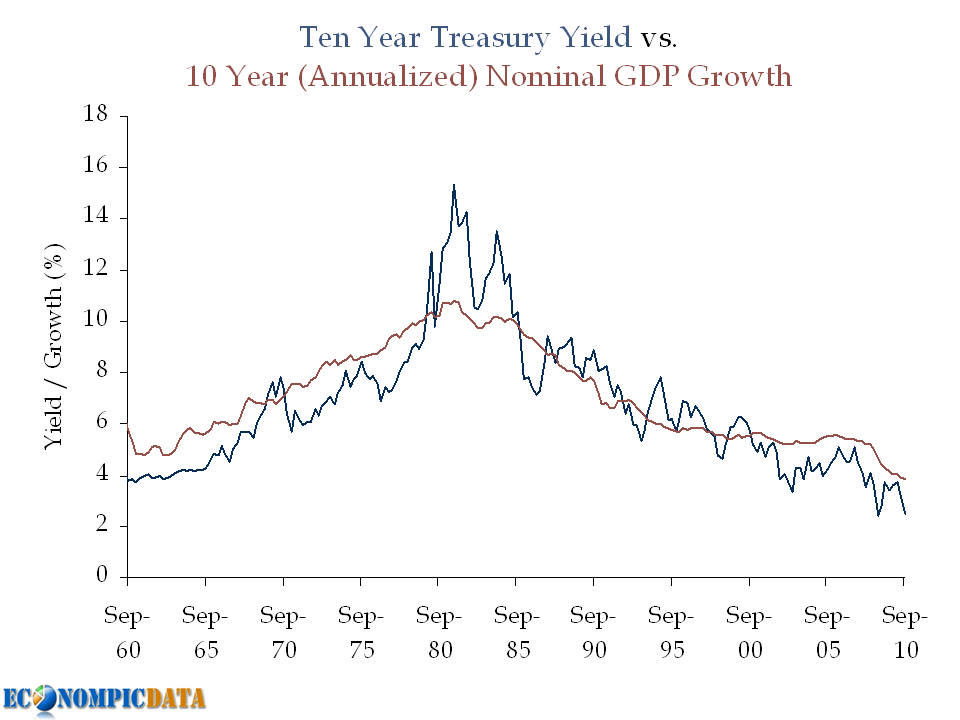

As ten year yields re-approach 2.7% levels, let us revisit (i.e. pat myself on the back for) a post from last September when yields were 2.7%.

On the Value of Treasuries - September 7th, 2010

In recent weeks, a number of investors I respect have commented that Treasuries are rich and should be avoided (or even outright shorted). Recent examples include Doug Kass and James Montier, both of whom claim current yields put too much weight on expectations of a double dip. I simply don't agree...

While I am not a Treasury bull, it is my view that at a 2.7% yield Treasury bonds are fairly valued when one takes into account the low growth / low inflation outlook, the Fed's extended easing policy, and the potential for capital appreciation rolling down the steep yield curve. Below we'll take a look at these three points in more detail.

Point #1) Nominal Growth Matters

This point was first shown in the following chart a few weeks ago.

In Doug's post he compares historical real GDP to Treasury yields and notes that bonds should be yielding more (he notes that Treasuries have historically yielded ~360 bps more than real GDP). The problem with this analysis outside of an apples (real GDP) to oranges (nominal Treasury yield) approach, is that a large portion of this "spread" was due to the inflation spike seen in the chart above during the late 1970's / early 1980's; a period marked by high nominal Treasury yields and low real GDP.

Point #2) The Importance of Monetary Easing Policy

A bond investor that does not take duration risk can only earn VERY low rates over the next few years as long as the Fed is on hold. If an investor earns VERY low rates for each of the next two years, they will need to earn a much higher return for the remaining 8 years just to break-even with the Treasury investment. The key is that the market is pricing this in.

Example:

Assuming a "zero" interest policy for two years (by zero, lets assume 0.25%), this means that a 2.7% yield can be achieved as follows:

- The first 2 years at 0.25%

- The last 8 years at 3.32%

The chart:

The relevance? The market is not forecasting rates will stay as low as they are now (i.e. forward rates are higher... closer to that 3.32% rate than 2.71%), which means capital losses will not happen simply if rates rise from current levels, but rather rise above levels expected by the market going forward.

Point #3) Don't Forget the Rolldown

The yield curve is VERY steep (i.e. upward sloping). This means that the 10 year bond will not only return its yield over the next 12 months if nothing changes (i.e. if the yield curve is exactly where it is today in 12 months), it will return more.

How much more?

Using current figures, the 10 year Treasury is yielding 2.71% while the 9 year Treasury is yielding 2.54% (17 bps difference). Assuming that nothing changes, performance of a 10 year bond over the next 12 months will be made up of the 2.71% yield plus the capital appreciation from moving from a required yield of 2.71% to 2.54% (i.e. a bond with a 2.71% coupon and a required yield of 2.54% will be worth more than par). This specific 17 bp move would add an additional 1.5% (assuming a duration of 8.75 years on a ten year Treasury) over the next 12 months, which means a 4.2% return for the 10 year note if nothing changes.

Source: Federal Reserve / BEA

U.S. Economy Firing on No Cyclinders

As Calculated Risk points out:

Not only has growth slowed, but the recession was significantly worse than earlier estimates suggested. Real GDP is still not back to the pre-recession peak.

The chart below shows the rolling three year average contributions by consumption, investment, government, and net exports... all of which combine for a real GDP lower than the level seen three years ago.

Q2 GDP... Where's the Consumer?

Bloomberg details:

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 1.3 percent in the second quarter of 2011, (that is, from the first quarter to the second quarter), according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 0.4 percent.

The acceleration in real GDP in the second quarter primarily reflected a deceleration in imports, an upturn in federal government spending, and an acceleration in nonresidential fixed investment that were partly offset by a sharp deceleration in personal consumption expenditures.

Source: BEA

Wednesday, July 27, 2011

With a Treasury Closer to Default....

The only ETF on the daily screen I run from time to time in positive territory... Treasuries!

Source: Yahoo Finance

Tuesday, July 26, 2011

Buying Options

The U.S. may or may not default on its debt (I am going with the not), may or may not be downgraded (I think it is likely within the next 12 months), and may or may not be a completely dysfunctional mess in Washington (okay, this is a definite). In times like this, I would like optionality (calls and puts) even if it were expensive.

But, lo and behold... the VIX is currently priced below its 5, 10 and 20 year average.

Which is why I am buying options....

Source: Yahoo Finance

Friday, July 22, 2011

Breaking Down the GLD / SPY Model

I've been researching and analyzing a number of rotation / momentum strategies of late (details potentially to follow), which is one reason why I was so interested in the recent GLD / SPY Rotation Strategy posted by Michael Gayed over at The Big Picture. In a nutshell the strategy attempts to follow rolling monthly momentum to allocate between gold and the S&P 500. He concludes:

Of course, past performance is not indicative of future results, but the simple binary decision of being either long SPY or long GLD depending on which is outperforming the others does seem to suggest alpha can be generated.

While I am not nearly as willing to suggest the framework works (and if it does, it doesn't necessarily work in the manner described), I did think the framework was interesting enough to take a deeper dive.

First of all, let's outline the strategy:

I was able to closely match the results:

What I Like

Before I dive into the issues I have with the analysis, here is what I like...

I like that while the strategy was only allocated to gold about 50% of the days, it still tracked the performance of gold with a correlation of .70 on a monthly basis. That is pretty staggering. Why do I like that? Because it opens up the possibility that it closely tracks gold when gold outperforms and may track equities when equities outperform.

Issues

That said, here are my main issues with the model:

- The data set is very limited

- The data is from a period in which gold significantly outperformed equities

If you were to have asked me prior to seeing the analysis if I was interested in a model that involved gold and equities that outperformed equities over the past 6 1/2 years, my response would have been a very easy no. Unless the model shorted gold, it would have been just about impossible NOT to outperform equities over that time frame (gold is one of the top performing asset classes since 2004; equities one of the worst).

As a result, I would have been much more interested in hearing about a model that outperformed gold over this time, rather than consistently underperform over its history (20.7% annualized returns vs. 17.9% annualized returns), without much of a reduction in volatility (21.1% vs. 20.3%).

Deeper Dive

Keeping those limitations in mind, lets dive into the idea that gold is a good momentum strategy. The below chart summarizes the performance of the model based on different periods of exhibited "strength" in the model as defined by the level that the GLD / SPY index was above its 20 day moving average and the corresponding one day forward average return in the price of gold and the S&P 500.

An interesting observation is that the only level that gold did not outperform was when the GLD / SPY index was greater than 10% above the 20 day moving average (note that this was less than 2% of all trading days) and GLD / SPY outperformed most when the GLD / SPY index was more than 10% below the 20 day moving average. This:

- Indicates the GLD / SPY index outperformed the S&P 500 because gold in most instances outperformed the S&P 500

- The model actually shows gold and S&P 500 exhibit mean reversion at extreme levels

Update:

I was able to find Gold prices going back to 1992 (the inception of the SPY) over at USA Gold and recreated the model using Gold rather than GLD. The results don't seem too promising prior to the beginning of the gold rally that started in 2001.

Source: Yahoo Finance

Thursday, July 21, 2011

Monday, July 18, 2011

Silver is Once Again on a Tear

Similar to gold (see a past post On the Value of Gold) silver has been on a tear due to low interest rates, fear of inflation, and a declining dollar (actually not similar to gold, but more like in multiples greater than gold). While the price of gold or silver is already a reflection of a weak dollar (i.e. if silver increases in price, it is outperforming the dollar), the relationship between the dollar index (relative to other currencies) and silver since the beginning of the year has been rather striking.

The warning note to the above is that while this relationship is not new, the scale of the relationship of ~10x since last summer, is (from 2007-mid 2010 it was closer to 2x).

Source: Yahoo Finance

The warning note to the above is that while this relationship is not new, the scale of the relationship of ~10x since last summer, is (from 2007-mid 2010 it was closer to 2x).

Perhaps this time is different and we should simply be Ready to Ride the Golden Silver Bubble.

Source: Yahoo Finance

Monday, July 11, 2011

Market Smack-Down

In the battle of technicals vs fundamentals, on this day fundamentals are winning.

I just dipped my feet back in the water with some calls on the S&P. While vol has spiked today, a level below 20% considering everything going on in the world seems cheap and indicates the market may prefer to move higher. No way I (personally) would be buying outright here though.

Source: Yahoo Finance

Friday, July 8, 2011

Hours Worked per Person Flatlining

Hours Worked per Person (Employment to Population Ratio x the Average Work Week of Private Workers), shows the sluggish rebound in "labor usage" relative to the population.

The concern... for the last 25 years there has been a very strong relationship between hours worked per person and real GDP growth (a decent relationship prior to 1986, but with a lot more noise), but notice the huge gap since the "recovery" began.

Unless "this time is different" there are two possibilities:

- The Good: Employment will follow (it just needs an unprecedented amount of time)

- The Bad: The economy is outperforming due to all the government support / transfer payments, the impact of which will be fading going forward

No Good News in Employment Report

The LA Times reports:

Analysts had raised their job-growth forecasts for June to 100,000 or more in recent days, hopeful of a rebound after surprisingly few job gains in May, which many attributed to temporary factors such as Japan's earthquake and the spike in oil prices.

But, in fact, the growth of 54,000 jobs previously reported for May was revised down Friday to just 25,000. And the nation's payrolls followed that with a barely perceptible 18,000 new net jobs last month.

Friday’s jobs report was remarkable in that there was nothing positive in it. Manufacturing, instead of bouncing back up as many had expected, added a meager 6,000 jobs. Hiring in construction remained dismal. The once-fast-growing temporary-help industry shed jobs for the third month in a row. And budget-strapped government offices eliminated an additional 39,000 jobs from their payrolls. Services remained weak.

Even for those with jobs in June, there was bad news. The average weekly work hours declined by 0.1 to 34.3. And the average hourly earnings for all private-sector employees dropped by one cent to $22.99.

Things are even worse if you look at the Household survey (the survey used to determine the unemployment rate), where more than 440,000 jobs were lost during the month as individuals are flying out of the workforce. That figure takes into account the 59,000 teenagers finding jobs (not exactly the high paying jobs).

Source: BLS

Thursday, July 7, 2011

ADP Employment Better than Expected

CNN details:

Payroll processing company ADP said private jobs grew rapidly in June -- a figure that was much higher than expected and more than four times higher than the prior month. May's figures were downwardly revised to 36,000 jobs. Economists were expecting a gain of just 60,000 private sector jobs, according to consensus estimates from Briefing.com. Smaller businesses led the charge in June. Small businesses, defined as those with fewer than 50 workers, added 88,000 jobs in June. Medium-size businesses, defined as those with between 50 and 499 workers, gained 59,000.Don't get me wrong, a better figure is good news, but let's put this in perspective.

Source: ADP

Wednesday, July 6, 2011

ISM Employment Improving... But Lacking Snap Back

As we wait for the ADP employment figure this morning (not sure why its delayed), below is a chart summarizing the ISM Manufacturing and Services employment indices with the total number employed.

Friday, July 1, 2011

Equity Valuation Based on GDP Growth

An update (with a small addition) of a post from May 2010

Step 1) Take the S&P 500 Index (lots of data here) and divide that level by the current level of nominal GDP (you can find that here).

Below is a chart of just that going back to 1951 and the corresponding 60 year average.

Step 2)

Fair Value Methodology: Take that 60 year average (8.25%) to normalize the first year of your 'Fair Value S&P 500' "FV" Index by taking nominal GDP at the starting date (in this case June 1951 = $336.6 billion) and multiplying by the percent (x 8.25% = 27.77). In this case 27.77 = the FV Index level (or the starting value normalized).

Matched Starting Value Methodology: Simply start the index at the value of the S&P 500 as of June 1951 = 21.55.

Step 3) Using that 27.77 (or calculated value using a different time frame) as the FV Index starting value or 21.55 as the matched starting value, at each interval increase the index by the change in nominal GDP (note... in the chart below, I estimated the Q2 GDP at 2.0% annualized). Why nominal GDP? Go here.

The below chart shows these calculated indices vs the actual S&P 500 index.

Step 4) Calculate the percent the S&P 500 Index is over or under valued relative to each calculated index.

Relationship (returns are annualized)....

Note 1: under these methodologies, the S&P 500 is currently at or above fair value, still implying a decent ten year forward change in the S&P 500 plus dividends minus inflation.

Note 2: a change in the starting value of the FV Index would simply shift the x-axis to the right or left (i.e. it would not change the relationship between the two)

Source: Irrational Exuberance

Thursday, June 30, 2011

Chicago Manufacturing Beats Expectations

The WSJ Blog details:

U.S. manufacturing activity was stronger than expected in June, with rising orders and easing price pressures, according to the monthly survey of Chicago-area purchasing managers.

The closely-watched Chicago Business Barometer broke three months of slowing growth in June, rising to a seasonally-adjusted 61.1 from 56.6 in May, well above the 53.5 consensus among analysts surveyed by Dow Jones Newswires.

Chicago PMI: Index > 50 = Expansion

Another important detail from this months report was the decline in inventories, which infers that manufacturers will need to produce more to meet demand (they met a portion of current demand simply out of inventories), a good sign for future growth.

Source: ISM

Thursday, June 23, 2011

How We're Chillin...

When I took a look at the difference in the amount of leisure between those employed / unemployed and educated / uneducated, I was reminded of the old adage "cash rich, time poor". And apparently I watch a LOT less TV than most (actually... this may average out during football season) and spend WAY too much time on the computer.

Source: BLS

Source: BLS

New Home Sales Flatlines

Reuters details:

The Commerce Department said May new home sales fell 2.1 percent to a seasonally adjusted annual rate of 319,000. Analysts polled by Reuters were expecting a slightly slower pace of 310,000 for the month.Lets take a look at those recent "strong gains" by sale price.

The decline ended two straight months of strong gains, with sales rising 6.5 percent in April and 8.9 percent in March. May's new home sales were 13.5 percent above the May 2010 level.

And relative to the longer term by region (note that "strong gains" in percent terms are easy when the base is 80% below previous peaks).

As GYSC noted in a previous post:

I cannot believe how many run thier game under "The FED is behind us no matter what!".While that is a great trade when the market simply needs liquidity, as seen above it doesn't help so much when the asset has fundamental issues.

Source: Census

Wednesday, June 22, 2011

Suppressed Yields?

In a recent post titled Suppressed Volatility, EconomPic posited:

That's right. In the first quarter, the Fed purchased $1.4 trillion in Treasury securites or 190% of all net issuance for the quarter (a period in which households reduced Treasury holdings by more than $1 trillion). This $1 trillion went somewhere (think risk assets). Also would seem to explain why Treasuries snapped back sharply in the second quarter when disappointing economic news and a subsequent rebound in demand for Treasuries was met by a reduced net supply.

Source: Federal Reserve

It is simply (in my view) that volatility across ALL sectors and asset classes has been suppressed by the liquidity that has successfully (to date) been finding its way into riskier and riskier asset classes following the combination of unprecedented fiscal / monetary stimulus and a lack of "real" investments (i.e. investments that feed into economic growth and create jobs) for this liquidity to go.Here is a visual depiction of that mechanism.

That's right. In the first quarter, the Fed purchased $1.4 trillion in Treasury securites or 190% of all net issuance for the quarter (a period in which households reduced Treasury holdings by more than $1 trillion). This $1 trillion went somewhere (think risk assets). Also would seem to explain why Treasuries snapped back sharply in the second quarter when disappointing economic news and a subsequent rebound in demand for Treasuries was met by a reduced net supply.

Source: Federal Reserve

Tuesday, June 21, 2011

Suppressed Volatility

FT Alphaville has a post Crouching Vix, Hidden Volatility claiming that:

Volatility is out there. You just have to look for it — and not by glancing at industry-standard, the CBOE Vix index.

The blog then points to a post by ConvergEX that states:

If you only focused on the CBOE VIX Index, you’d be tempted to think that the recent market volatility was pretty modest.

The problem is that it wouldn't only be a temptation, it would be a fact.

Looking at implied volatility, as defined by the VIX, relative to actual realized three month volatility of the S&P 500, the VIX has (much like most of history) been consistently overstating volatility (the VIX recently closed at 19 vs. three month realized volatility of 12, a difference of 7 relative to the average difference of 4 over the previous 20 years).

This isn't to say that I believe the VIX accurately reflects the economic environment and risks associated with investing in the current environment (I absolutely don't). It just isn't some conspiracy theory that the VIX is being artificially suppressed relative to the underlying market or that volatility is more accurately reflected in other sectors.

It is simply (in my view) that volatility across ALL sectors and asset classes has been suppressed by the liquidity that has successfully (to date) been finding its way into riskier and riskier asset classes following the combination of unprecedented fiscal / monetary stimulus and a lack of "real" investments (i.e. investments that feed into economic growth and create jobs) for this liquidity to go.

So tread carefully my investment friends. The part of the investment cycle where an investor can generate positive returns by simply providing liquidity to the market is likely over.

Source: Yahoo Finance

Friday, June 17, 2011

Leading Indicators Bounce

With everything going on in Europe, this release feels worthless, but here it is anyway.

Source: Conference Board

Wednesday, June 15, 2011

Foreigners Still Buying Treasuries

I'm reminded of the quote "Cleanest dirty shirt". Bloomberg details:

China, the largest foreign owner of U.S. government debt, added to its holdings for the first time in six months in April as economic data weakened and the Federal Reserve signaled no extension of its $600 billion purchase plan.

Chinese officials, as well as those in Germany and Brazil had been critical of the Fed’s asset purchase plan when it was first announced in November, said the proposal would be inflationary and could hurt the value of dollar-denominated assets. The Fed became the largest owner of Treasuries through what has become known as its policy of quantitative easing, in which bonds were bought to add cash into the economy and reduce the risk of deflation. The purchases end this month.Also of note (and outlined previously at EconomPic here):

Even with the increase, the data “underestimates what China’s buying,” said Scott Sherman, an interest-rate strategist at Credit Suisse Group AG in New York, a primary dealer. “China deals through foreign intermediaries” leading to initial tallies counting their purchases as belonging to other holders, such as the U.K.Hence the China and United Kingdom aggregation below.

Source: Treasury

Tuesday, June 14, 2011

Producer Prices Moderate in May, Highest Year over Year Level Since September 2008

Marketwatch details:

Source: BLS

U.S. wholesale prices rose in May at the slowest pace in 10 months as the cost of food fell and the increase in energy prices tapered off, the government reported Tuesday.Over the longer term, easy money policy sure is working at the producer price level with finished goods increasing 7.3% year over year, the highest level since September 2008. One issue is that the easy money isn't feeding into demand / price increases for labor (likely because it is so focused at the producer levels, rather than the consumer level where corporations can pass on price increases) so the below acts as an added tax on goods used as inputs.

The producer price index rose 0.2% last month, the Labor Department said. It was the smallest gain since July 2010.

Food costs dropped 1.4%, owing mainly to lower vegetable prices, to mark the biggest one-month decline in almost a year. The price of food has fallen twice in the past three months, although food costs are still 3.9% higher compared to one year ago.

Energy prices, meanwhile, rose 1.5% in May, the slowest rate since September. A surge in fuel costs have push wholesale prices sharply higher since last fall, but oil prices have pulled back over the past month. Many economists expect the modest decline in oil prices to ease pressure on wholesale costs.

Source: BLS

Retail Sales Decline, but Beat Expectations

Reuters details:

Source: Census

Retail sales fell in May for the first time in 11 months as receipts at auto dealerships dropped sharply, but the decline was less than expected, offering hope of a pick-up in economic activity.Below are the details. While any given month is potentially just noise, it is interesting to see the largest declines in "big purchases" including autos, furniture, and electronics while healthcare, food services (i.e. eating out), and clothing grew.

Retail sales last month were depressed by a 2.9 percent drop in sales of motor vehicles, the largest decline since February 2010, as a shortage of parts following the earthquake in Japan left inventories lean and prompted manufacturers to raise prices.

Excluding autos, retail sales rose 0.3 percent last month, the smallest gain since July, after rising 0.5 percent in April.

Source: Census

Thursday, June 9, 2011

Trade Balance Improves in April

The WSJ details:

The U.S. deficit in international trade of goods and services declined 6.7% to $43.68 billion from a downwardly revised $46.82 billion the month before, the Commerce Department said Thursday. The March trade gap was originally reported as $48.18 billion.In other words, expect the fall in both the demand and the price for oil to continue to reduce the trade balance going forward in both real (due to demand) and nominal (due to price) terms.

The April deficit was much smaller than Wall Street expectations, with economists surveyed by Dow Jones Newswires having predicted a $48.3 billion shortfall.

A rebound in oil prices to levels not seen since the 2008 spike erased the modest reduction in the trade gap from late last year. But Nymex crude futures have settled back to around $100 a barrel after surging to nearly $115 a barrel in early May.

And over the longer run...

The below chart compares April 2010 and April 2011 trade balances* for a number of items in real terms.

Note the big improvement in industrial supplies (though this may be due to the disruption in Japan - a drop of $3.2 billion in imports came from March alone) and the big jump in consumer goods imports. The latter is a trend I imagine will continue as consumers look for cheaper and cheaper goods that are increasingly produced outside of the U.S.

Not broken out is trade in oil, which improved greatly in real terms; exports up by $700 million, imports down by $2 billion (the problem is the price more than made the trade balance worse in nominal terms).

Source: Census

Monday, June 6, 2011

Federal Debt per Employee

This will be the last employment related chart for a while (I think) following recent posts This Time IS Different... Employment Edition and Breaking Down Productivity. This specifically outlines a much broader issue that will affect us over the long-term. Specifically, the level of U.S. debt and the number of workers available to pay down that debt.

The amount of debt per employed person has spiked in recent years to more than $100,000 per employed worker, up from ~$55,000-$60,000 throughout the 1990's.

There are a number of ways this problem can be solved / corrected:

- Economic growth (good)

- Higher taxes (not bad depending on your point of view, but not good for underlying growth expectations of the U.S. economy)

- Decrease government spending (good IMO, but also not good for underlying growth expectations of the U.S. economy)

- Inflation (decrease the "real" value of debt via a "tax" to savers / earners unable to keep up their returns / wages with inflation)

- Outright default (not feasible)

All that said, debt deflation is still a major concern of mine due to the levels of debt and political grandstanding currently taking place in D.C. See Steve Keen's epic piece that changed my understanding of the economic collapse here for more on this possibility.

Source: Treasury Direct / BLS

Great Depression Employment Situation

In response to my post This Time IS Different, reader DIY Investor asked to see the information EconomPic presented, but for the Great Depression. Here you go...

The key takeaway... things were WAAAAAYYYYY worse than the recent 6% drop. Note (however) the rather remarkable snap back post 1933. The result is that within 10 years following the start of the Great Depression, employment was within 4% of the previous peak (and was positive year 11). Sadly, not too dissimilar to the -2% reduction in private employment we have seen over the last 10 years.

Source: U-S History

Friday, June 3, 2011

EconomPics of the Week (June Gloom Edition)

Lots of economic data was released this week and it was pretty much consistently bad (or at least disappointing).

On the investment front, that is partially offset by a crowd turning VERY bearish (normally a sign to buy). Not bearish enough for me though... similar to what I've done in the past when unsure, I am reigning it in BIG time. Almost all of my risk taking is through relative value trades (i.e. everything is at least partially hedged) and options (happy to pay sub 20% vol on calls to get my long equity beta exposures).

Here were those economic events as reported here at EconomPic.

This Time IS Different... Employment Edition

Breaking Down Productivity

Japanese Autos Crushed

Pace of U.S. Recovery Slowing

Gas Rules Everything Around Me

Chicago PMI Misses

And the video of the week... let's slow it down with Iron and Wine's 'Such Great Heights' (cover of a great / very different sounding Postal Service tune).

This Time IS Different... Employment Edition

Not different from past financial crises, but certainly different from recessions over the previous 40 years.

The first chart should look similar to other charts presented on the blogosphere. It shows the change in the total number of employed during past recessions. The key takeaway... this time is worse, but things are improving (albeit slowly).

The next chart shows how much worse. It takes the same data as the chart above, but shows the relative performance of this recession as compared to past recessions. For example, as compared to the last recession we are now trailing the employment situation by about 6.5% (we currently have 4.5% less jobs than our previous peak, while at this point following the 2001 recession we had 2.1% more jobs).

The concerning thing is that things seem to be getting worse, even though it "should be" easier to improve following a severe downturn (hiring back workers is typically easier than creating new jobs).

Seems more and more like a structural issue that cannot be addressed by simply trying to stimulate aggregate demand.

Source: BLS

Thursday, June 2, 2011

Breaking Down Productivity

Bloomberg details:

The first chart below shows total productivity broken out between its two components... hours worked and output per hour (you can only increase productivity by increasing one or the other).

Rolling One Year Change

A few points to notice... the snap back post recession was relatively small as compared to past downturns (especially considering how far things fell - a rebound to trend would have appeared especially large in itself) and the pace of productivity growth is slowing.

Rolling Five Year Change

The longer term trend above shows why we are feeling so much pain; we are at a multi-generational low in total productivity, almost entirely driven by the unprecendented decrease in hours worked.

The productivity of U.S. workers slowed in the first quarter and labor costs rose as companies boosted employment to meet rising demand.Let us dive into the numbers...

The measure of employee output per hour increased at a 1.8 percent annual rate after a 2.9 percent gain in the prior three months, revised figures from the Labor Department showed today in Washington. Employee expenses climbed at a 0.7 percent rate after dropping 2.8 percent the prior quarter.

“Productivity growth has slowed in the past year but from very strong rates and it remains fairly decent,” Sal Guatieri, a senior economist at BMO Capital Markets in Toronto, said before the report. “Labor costs have moved higher because of the slowing in productivity growth, but they were generally falling for some time and remain very weak, essentially implying no threat to the inflation outlook.”

The first chart below shows total productivity broken out between its two components... hours worked and output per hour (you can only increase productivity by increasing one or the other).

Rolling One Year Change

A few points to notice... the snap back post recession was relatively small as compared to past downturns (especially considering how far things fell - a rebound to trend would have appeared especially large in itself) and the pace of productivity growth is slowing.

Rolling Five Year Change

The longer term trend above shows why we are feeling so much pain; we are at a multi-generational low in total productivity, almost entirely driven by the unprecendented decrease in hours worked.

The next chart outlines (in my opinion) the bigger story. It is the change in the productivity to hours worked ratio over rolling ten year periods. As an example of how to interpret the chart, the most recent period shows a change of around 40%. What this means is that productivity has grown by about 40% relative to hours worked over the past 10 years (they've grown 30%, while hours are down about 8%). This is by far a multi-generation high.

This helps explain a lot of the current situation. While productivity in itself is not a bad thing at all (in fact, I would argue it is one of the most important things for sustained economic growth), when productivity is increasing solely to offset hours worked, a lot of structural imbalances result UNLESS there is policy (education, reallocation from those that benefit to those that suffer, etc…) that helps transition the broader economy to a new “balance”. If this does not happen, workers replaced with new productive resources find themselves not only suffering personally, but dragging the economy down as they are no longer adding to the hours worked component of productivity (as I mentioned, it is one of only two inputs).

The other important question is whether the productivity is truly an increase in productivity or just a shift in the hours worked component from the U.S. to those abroad. As I’ve outlined here, over the last 10 years (i.e. when the output / hours worked ratio spiked in the chart above) there was a huge labor supply shock coming from emerging Asia. My concern is that we are not really becoming all that more productive with new technologies, process, etc..., but simply outsourcing a lot of the hours worked overseas. This would explain a ton, including the strength of emerging Asia relative to the U.S., the disparity between “haves” and “have nots” by educational attainment (i.e. the economic slump has been felt to a much greater extent by those with less education whose jobs have been exported), and the soaring profits by corporations even in the face of lower growth (cutting costs vs. increasing revenues).

Source: BLS

This helps explain a lot of the current situation. While productivity in itself is not a bad thing at all (in fact, I would argue it is one of the most important things for sustained economic growth), when productivity is increasing solely to offset hours worked, a lot of structural imbalances result UNLESS there is policy (education, reallocation from those that benefit to those that suffer, etc…) that helps transition the broader economy to a new “balance”. If this does not happen, workers replaced with new productive resources find themselves not only suffering personally, but dragging the economy down as they are no longer adding to the hours worked component of productivity (as I mentioned, it is one of only two inputs).

The other important question is whether the productivity is truly an increase in productivity or just a shift in the hours worked component from the U.S. to those abroad. As I’ve outlined here, over the last 10 years (i.e. when the output / hours worked ratio spiked in the chart above) there was a huge labor supply shock coming from emerging Asia. My concern is that we are not really becoming all that more productive with new technologies, process, etc..., but simply outsourcing a lot of the hours worked overseas. This would explain a ton, including the strength of emerging Asia relative to the U.S., the disparity between “haves” and “have nots” by educational attainment (i.e. the economic slump has been felt to a much greater extent by those with less education whose jobs have been exported), and the soaring profits by corporations even in the face of lower growth (cutting costs vs. increasing revenues).

Source: BLS

Wednesday, June 1, 2011

Japanese Autos Crushed

The WSJ details:

The Japanese auto makers were hit hardest, but nearly all major auto makers reported declines from a year ago. GM's sales fell 1.2% while Ford Motor Co. said its May U.S. sales declined less than 1%. Toyota's sales dropped 33%, Honda's sales fell 23% and Nissan Motor Co.'s dropped 9.1%.

Chrysler's sales rose 10.1%, giving the company a 10.9% shares of the U.S. market, putting it ahead of Toyota, which had a 10.2% share. GM, Ford and Chrysler together accounted for 49.7% of the month's sales. The last time they had more than 50% was September 2008.

Hyundai capitalized on a lineup that has the highest combined fuel efficiency of any in the industry and attractive prices relative to competitors. The South Korean auto maker has pulled drawn customers from Toyota, Honda and Nissan, which suffered production disruptions because of the March 11 earthquake in Japan.

Since the Japanese earthquake / Tsunami on March 10th, Hyundai's stock price has soared by more than 20%, while Toyota has slumped 7%.

Source: Auto Blog

Pace of U.S. Recovery Slowing

Growth in the economy appears to be slowing (not that the recovery was all that amazing to begin with).

ISM Manufacturing

ADP Payroll (the "real" figure arrives this Friday)

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}

{kind=link}

{kind=link}