After a relaxing week that involved sitting on a beach, I expect posting to resume next week.

But, to leave you all with a song for the week... Foster the People with Helena Beat

After a relaxing week that involved sitting on a beach, I expect posting to resume next week.

The AP details:

Fixed mortgage rates have fallen to historic new lows for a fourth straight week and are likely to fall further.

The average on a 30-year fixed mortgage fell to 4.01 percent this week, Freddie Mac said Thursday. That's the lowest rate since the mortgage buyer began keeping records in 1971. The last time long-term rates were lower was in 1951, when most long-term home loans lasted just 20 or 25 years.

The average on a 15-year fixed mortgage, a popular refinancing option, ticked down to 3.28 percent. Economists say that's the lowest rate ever for the loan.

Mortgage rates tend to track the yield on the 10-year Treasury note. The 10-year yield has risen this week to around 2 percent. A week ago, it touched 1.74 percent -- the lowest level since the Federal Reserve Bank of St. Louis started keeping daily records in 1962. As recently as July, the 10-year yield exceeded 3 percent.

There are lots of reasons why equity markets have sprung back to life (and bonds have "normalized" away from lows) the past few days. The most front and center reasons include a potential European debt deal and the fact that markets were simply oversold (I agree on both fronts), but here is another... institutional rebalancing.

When prices are still up 45% (SLV) and 26% (GLD) over the past 12 months, I would call it a correction.

While leading economic indicators expanded 0.3% during August, the expansion remains focused on areas controlled by monetary policy rather than the underlying economy. For the third month in a row (and four of the past five), indicators outside the Fed's control were negative.

Over the past ten years (less so prior), the relationship between the change in the 10 year Treasury yield and the change in the S&P 500 has been strong with the 10 year Treasury leading. Note the breakdown in the relationship over the past year (perhaps due to Fed intervention).

Economic Data

Investments

Illusion of Prosperity presents an interesting chart outlining the stagnation is real per capita restaurant sales over the course of the past decade (hat tip GYSC). I wanted to take a deeper look.

What the below charts outline are real per capita retail sales for food services (i.e. restaurant) and food stores (i.e. food for home). The figures are the result of discounting the nominal retail sales by inflation (the BLS breaks out inflation data for both food at home and food away from home), as well as population growth.

The results...

The overall level of food consumed appears to be relatively sticky (right around $300 / person per month), though overall consumption is down by 5% in real terms since 1992. During that time there has been a sizable shift to eating out, which could mean the decline in real terms has to do with eating "cheaper" fast food.

Breaking out each component, we can clearly see the shift to eating out from 1992 to 2006. Since then, it is pretty amazing to see the drop in both components during the crisis and the subsequent rebound (albeit to levels below the previous peak) since.

While not a surprise, this is rather concerning. I recently outlined that bottom earners have been earning less for the better part of the past 15+ years and it looks like it may be actually impacting the dietary habits of Americans (i.e. eating less [unlikely] or eating cheap / unhealthy food [likely]).

Source: Census, BEA, BLS

The WSJ details:

Back in February, I outlined that retail sales data was extremely noisy during periods of volatile prices as the data is shown in nominal (rather than real) terms. As the chart below shows, the relationship between retail sales (again, a nominal figure) and commodity prices (as reflected by ETF DBC) is strong.Retail and food services sales were virtually unchanged from the previous month at an adjusted $389.50 billion, the Commerce Department said Wednesday.

Economists surveyed by Dow Jones Newswires had forecast a 0.3% increase. July retail sales were revised down to a 0.3% gain. The Commerce Department originally estimated 0.5%.

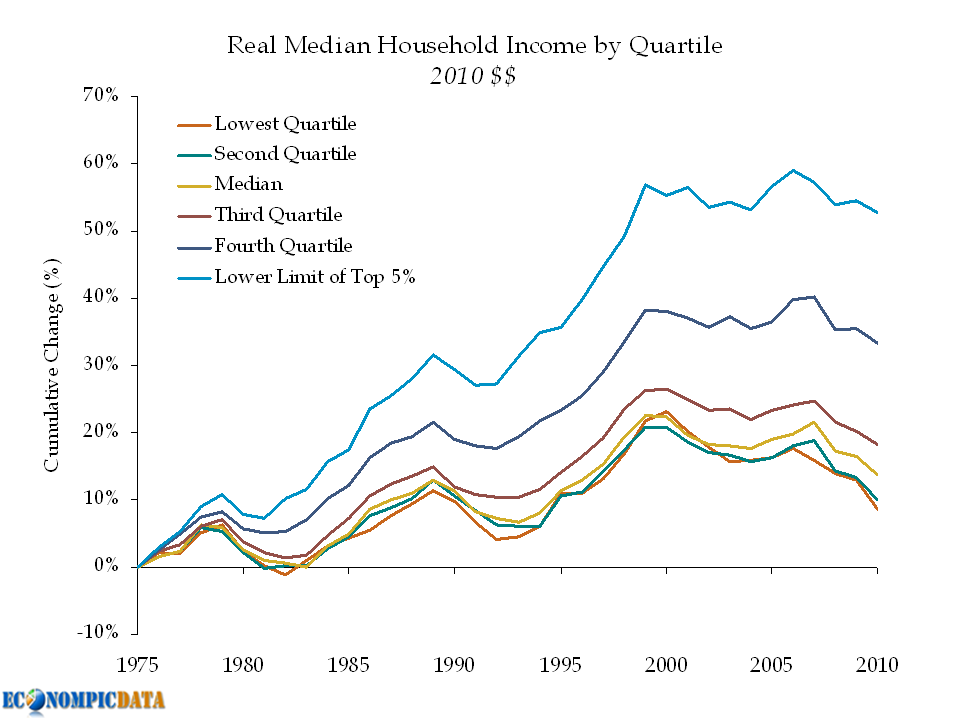

The income of the average American worker—long the envy of much of the world—has dropped for the third year in a row and is now roughly where it was in 1996, adjusted for inflation.

The U.S. poverty rate, meanwhile, has continued to rise. America's median household income—what the statistical middle of the pack earns in a year—fell 2.3% to $49,445, adjusted for inflation, according to the Census Bureau's annual snapshot of living standards. The figure has fallen each year since 2007 as high unemployment and a tougher job market has made it harder for working Americans to get bigger paychecks.

This downdraft is part of a longer trend that has wiped out the wage gains of the last decade. Inflation-adjusted household income is now down 7.1% from its peak in 1999, and 2010 is the first time since 1997 that American households made less than a median of $50,000.

"The past decade was just a mirage," says Justin Wolfers, an economics professor now visiting at Princeton University. That's because wage gains earlier in the decade were never that robust, yet people were able to take advantage of surging housing values and easy credit to spend more than they earned.

As someone who lived and worked very close to the World Trade Center ten years ago on that horrible day, I have been greatly impacted by those day's events even though I was extremely lucky to have not known any of the victims at the time. I wish everyone the best that was directly impacted that day and I am amazed by the resiliency of so many and of the city itself. I just hope that ten years from now we are able to look back and see a lot more positive things that may still come from dealing with the tragedy, as well as resolved some of the hate that resulted from that day. Even though I have recently left NYC, I will always be a New Yorker and I know the city still has its best to come.

Treasury debt prices rose on Friday, taking benchmark yields to the lowest in at least 60 years as investors looked for a safe haven on revived worries a European debt crisis could have a significant global impact.Note the "at least" 60 years. The chart below shows the ten year Treasury yield over the last 110 years combining monthly data from Irrational Exuberance and daily data from the Federal Reserve once available.

Bloomberg details:

Consumer borrowing in the U.S. rose by the most in more than three years in July, led by a gain in non-revolving credit that includes student loans.

Credit increased $12 billion after a revised $11.3 billion rise in June, the Federal Reserve said today in Washington. Economists projected a $6 billion gain, according to the median forecast in a Bloomberg News survey. The rise in non-revolving loans was the most since November 2001.

Revolving credit showed the biggest decrease in six months, indicating Americans may be cutting back on non-essential items as limited job and wage growth depresses consumer confidence. Employment and income gains may be required to help spark the household spending and the recovery.

Bloomberg details (the below was pieced together from a broader article):

The quits rate can serve as a measure of workers’ willingness or ability to change jobs. The number of quits (not seasonally adjusted) in July 2011 increased from 12 months earlier for total nonfarm, total private, and government. In the regions, the number of quits rose in the Midwest and West.

The layoffs and discharges level (not seasonally adjusted) declined over the 12 months ending in July for total nonfarm and government. The number of layoffs and discharges was little changed in all four regions over the year.

Asset Classes

The Predictive Power of "Stocks as Bonds"

Generation Vexed... Housing Edition

The Month that Was...

Economics

Happy Labor Day Everyone!!!!

August Employment Shows No Job Recovery

Consumer Confidence Smack Down... Jobs Edition

On the Response to Irene...

Real GDP per Capita at March 2005 Levels

Manufacturing at Stall Speed... Production and New Orders Decline

Why a One Size Fits All Policy Doesn't Work

Where's the Investment?

And your quote of the week (don't expect this to be a regular occurence... I just really liked this quote):

Great minds discuss ideas; Average minds discuss events; Small minds discuss people.-Eleanor Roosevelt

Labor Day is traditionally a time for picnics and parades. But this year is no picnic for American workers, and a protest march would be more appropriate than a parade.

Not only are 25 million unemployed or underemployed, but American companies continue to cut wages and benefits. The median wage is still dropping, adjusted for inflation. High unemployment has given employers extra bargaining leverage to wring out wage concessions.

All told, it’s been the worst decade for American workers in a century. According to Commerce Department data, private-sector wage gains over the last decade have even lagged behind wage gains during the decade of the Great Depression (4 percent over the last ten years, adjusted for inflation, versus 5 percent from 1929 to 1939).

The ratio of corporate profits to wages is now higher than at any time since just before the Great Depression.

I'll keep my comments brief... any way you cut it, the employment report was extremely weak. Off to a long weekend...

Household Survey - unlike the establishment survey, this actually showed jobs being added (reversing last month's figure which showed a decline)... just not as fast as labor force growth)

First, what are we looking at...

Highlights:

Bulls would say "if you believe at all in mean reversion, then the U.S. economy is bound to bounce back". Bears would say "this time truly is different and the recession didn't wipe out excesses (i.e. debt, imbalances between classes, etc...), thus we still have a way to go".

Source: Population / Real GDP

What respondents are saying:

Source: ISM

{kind=link}