Asset Classes

Economic Data

Random

And the EconomPic video of the week... a sick rendition of a great song. ThePETEBOX with a cover of the Pixies Where is My Mind?

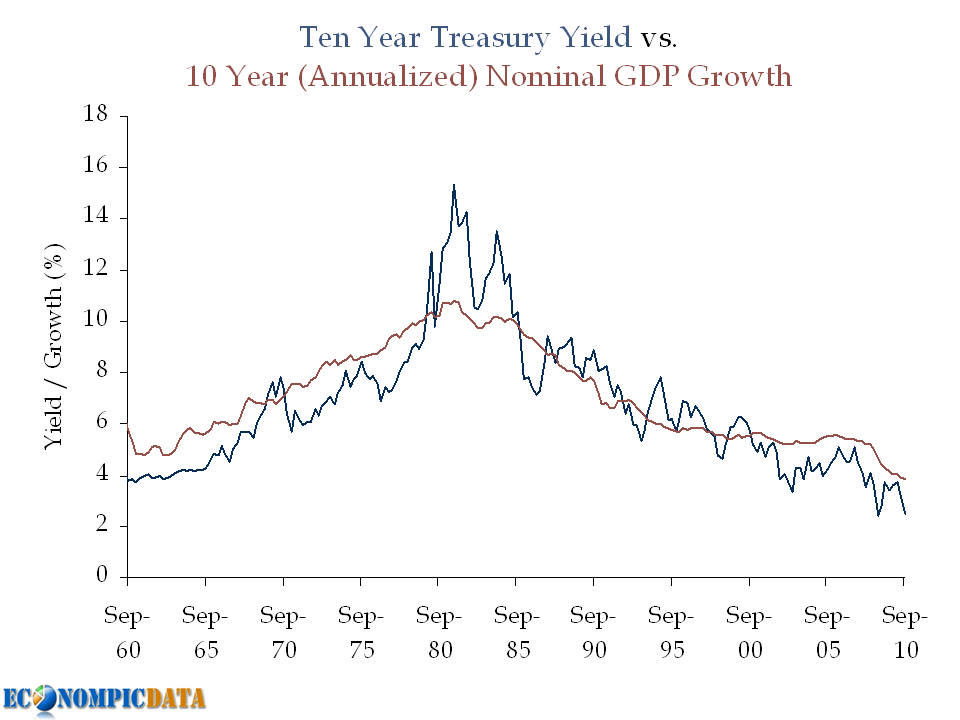

In recent weeks, a number of investors I respect have commented that Treasuries are rich and should be avoided (or even outright shorted). Recent examples include Doug Kass and James Montier, both of whom claim current yields put too much weight on expectations of a double dip. I simply don't agree...

While I am not a Treasury bull, it is my view that at a 2.7% yield Treasury bonds are fairly valued when one takes into account the low growth / low inflation outlook, the Fed's extended easing policy, and the potential for capital appreciation rolling down the steep yield curve. Below we'll take a look at these three points in more detail.

Point #1) Nominal Growth Matters

This point was first shown in the following chart a few weeks ago.

In Doug's post he compares historical real GDP to Treasury yields and notes that bonds should be yielding more (he notes that Treasuries have historically yielded ~360 bps more than real GDP). The problem with this analysis outside of an apples (real GDP) to oranges (nominal Treasury yield) approach, is that a large portion of this "spread" was due to the inflation spike seen in the chart above during the late 1970's / early 1980's; a period marked by high nominal Treasury yields and low real GDP.

Point #2) The Importance of Monetary Easing Policy

A bond investor that does not take duration risk can only earn VERY low rates over the next few years as long as the Fed is on hold. If an investor earns VERY low rates for each of the next two years, they will need to earn a much higher return for the remaining 8 years just to break-even with the Treasury investment. The key is that the market is pricing this in.

Example:

Assuming a "zero" interest policy for two years (by zero, lets assume 0.25%), this means that a 2.7% yield can be achieved as follows:

Not only has growth slowed, but the recession was significantly worse than earlier estimates suggested. Real GDP is still not back to the pre-recession peak.

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 1.3 percent in the second quarter of 2011, (that is, from the first quarter to the second quarter), according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 0.4 percent.

The acceleration in real GDP in the second quarter primarily reflected a deceleration in imports, an upturn in federal government spending, and an acceleration in nonresidential fixed investment that were partly offset by a sharp deceleration in personal consumption expenditures.

Of course, past performance is not indicative of future results, but the simple binary decision of being either long SPY or long GLD depending on which is outperforming the others does seem to suggest alpha can be generated.

Analysts had raised their job-growth forecasts for June to 100,000 or more in recent days, hopeful of a rebound after surprisingly few job gains in May, which many attributed to temporary factors such as Japan's earthquake and the spike in oil prices.

But, in fact, the growth of 54,000 jobs previously reported for May was revised down Friday to just 25,000. And the nation's payrolls followed that with a barely perceptible 18,000 new net jobs last month.

Friday’s jobs report was remarkable in that there was nothing positive in it. Manufacturing, instead of bouncing back up as many had expected, added a meager 6,000 jobs. Hiring in construction remained dismal. The once-fast-growing temporary-help industry shed jobs for the third month in a row. And budget-strapped government offices eliminated an additional 39,000 jobs from their payrolls. Services remained weak.

Even for those with jobs in June, there was bad news. The average weekly work hours declined by 0.1 to 34.3. And the average hourly earnings for all private-sector employees dropped by one cent to $22.99.

Payroll processing company ADP said private jobs grew rapidly in June -- a figure that was much higher than expected and more than four times higher than the prior month. May's figures were downwardly revised to 36,000 jobs. Economists were expecting a gain of just 60,000 private sector jobs, according to consensus estimates from Briefing.com. Smaller businesses led the charge in June. Small businesses, defined as those with fewer than 50 workers, added 88,000 jobs in June. Medium-size businesses, defined as those with between 50 and 499 workers, gained 59,000.Don't get me wrong, a better figure is good news, but let's put this in perspective.

{kind=link}