David Leonhardt at NY Times Economix (hat tip Calculated Risk) discusses the relationship between mortgage rates and housing prices:

Anyone who argues that home prices do not seem headed for another big decline will probably hear some version of this question. Interest rates are historically low right now. They will surely rise at some point. All else equal, higher rates should push home prices down.

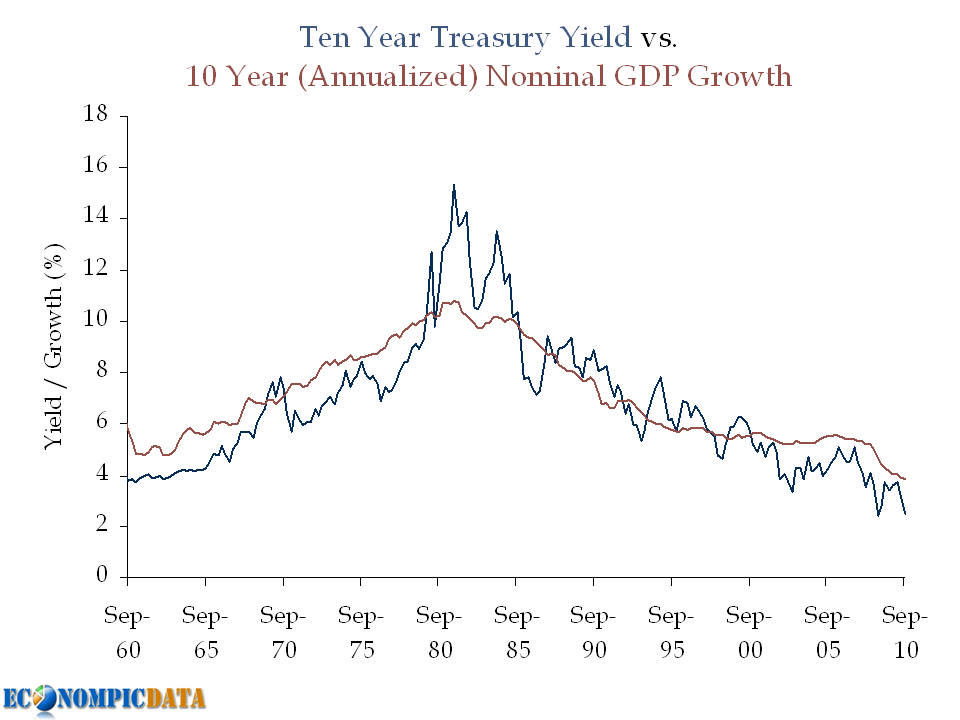

Yet compare the national median home price to 30-year fixed mortgage rates over the last three decades (with both indexed to 1 in 1971)

And shows the following chart:

And concludes:

It’s not easy to see much of a relationship. The fall in rates appears to have helped the housing boom of the last decade. On the other hand, the spike in rates in the 1980s had little apparent effect on prices. My best guess for why the two don’t correlate more closely is the role that psychology plays in housing markets. Prices just don’t move as quickly as economic theory suggests they should.

My immediate thought... why are you comparing REAL price levels with NOMINAL rates?

Lets see the relationship of real housing prices (in this case Case

Shiller discounted by CPI) vs. real mortgage rates less year over year CPI (note that the right y-axis is flipped to show the inverse relationship between the two).

A much stronger relationship appears when viewed on a real to real basis.

Note that the relationship appears to be non-existent from around 1972 to 1980 (pre-Case Shiller index data), which can be explained in part that government agency mortgages (i.e. subsidized financing rates that made housing affordable on a monthly payment rather than price level basis) jumped from just 10% of the market in 1980 to almost 50% by 2000 (see page 5 of the Fed's paper Securitization and the Efficacy of Monetary Policy for more).Calculated Risk seems to vehemently

disagree with my view that there is in fact a relationship between rates and price:

I've tried to explain this several times in several different ways. Price is what you pay for something. Interest rates are related to how the item is financed. Some people pay cash for a house. Would they pay more because interest rates are low? Nope.

My disagreement to his disagreement can be found in last month's post

The Importance of Mortgage Rates, but his argument is in a nutshell the following question:

Would people pay more for a car if interests rates are low?

My simple answer to that question... OF COURSE (and I did for my first car from a sleazy used car dealer).

Why? Because I could not afford to pay cash for the full price of a car at the time, thus I paid with credit, rather than fiat money (we live in a credit, not a fiat economy - see Steve Keen's epic piece that changed my understanding of the economic collapse

here for more).

Details of my first car purchase:

- 1990 Dodge Shadow (yikes)

- Cost: ~$3200

- Savings available for a car = ~$0

- Monthly disposable income available for a car = ~$100 / month

Without financing, I could not afford the

car I ended up with. With financing, I was able to afford it across a range of sticker prices, depending on financing rates, all at the same $100 / month payment. And unlike case-by-case deals on auto rates, anyone with decent credit and 20% down (harder to come by these days, but not limited) can access the subsidized mortgage rate.

Which brings me back to my conclusion in my post on

rates and housing:

Since the key contributor to housing affordability is not the current list price, but rather the mortgage rate, anyone looking to buy should seriously consider the alternative (i.e. renting) if they don't plan to use that contributing factor (again... the mortgage rate) for the life of the loan (i.e. to keep their house for 15-30 years).

If you do plan to buy a house for a smaller window of time (i.e. 1-10 years) with the idea of flipping it into a larger house, be careful. That per month clearing price may mean a much lower home value when you are trying to sell...

Source:

S&P,

BLS

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}